A while back I wrote about how Justin and I went from being $50k in the red to a net worth of zero. Today, I’m going to share how we paid off my student loans in 30 months.

Before I get too far, I need to share how much my student loan debt was and where it came from. (Warning: I briefly discuss an abusive relationship.)

how I paid for my education

Due to a series of poor choices, I didn’t actually start my college journey until the fall semester of 2004 – two years after I graduated from high school. When I did start going to college, I enrolled part-time at my local community college in Arizona and I majored in chemistry with plans of becoming a pharmacist. I was married to my first husband and worked for Wells Fargo as a home equity mortgage processor. Community college tuition was SUPER cheap, with most semesters were costing under $1,000 total. I was able to cash flow paying for school and keeping up on the rest of my bills (including my mortgage). Things got really ugly between me and my former spouse. It’s hard to talk about, but he would do everything he could to make sure that I knew that school wasn’t a priority for him including taking and hiding my books, purposefully making me late for class or work, and sabotaging my vehicle. (That’s the G-rated version…) I ended up moving in with my mom and filing for divorce.

While living with my mom, I started going to school full-time and continued working part-time. For all of its faults, Wells Fargo was very supportive of my school schedule. I worked mornings Monday through Friday and attended classes in the afternoons and evenings. As a result of the divorce, I needed to sell the house and split the proceeds. Luckily, the house had appreciated by about $75k due to the housing bubble that eventually got us the Great Recession. In hindsight, I’m so happy to have been on the right side of that disaster. I netted about $36k. I used some of the money to buy my Aveo and saved the rest.

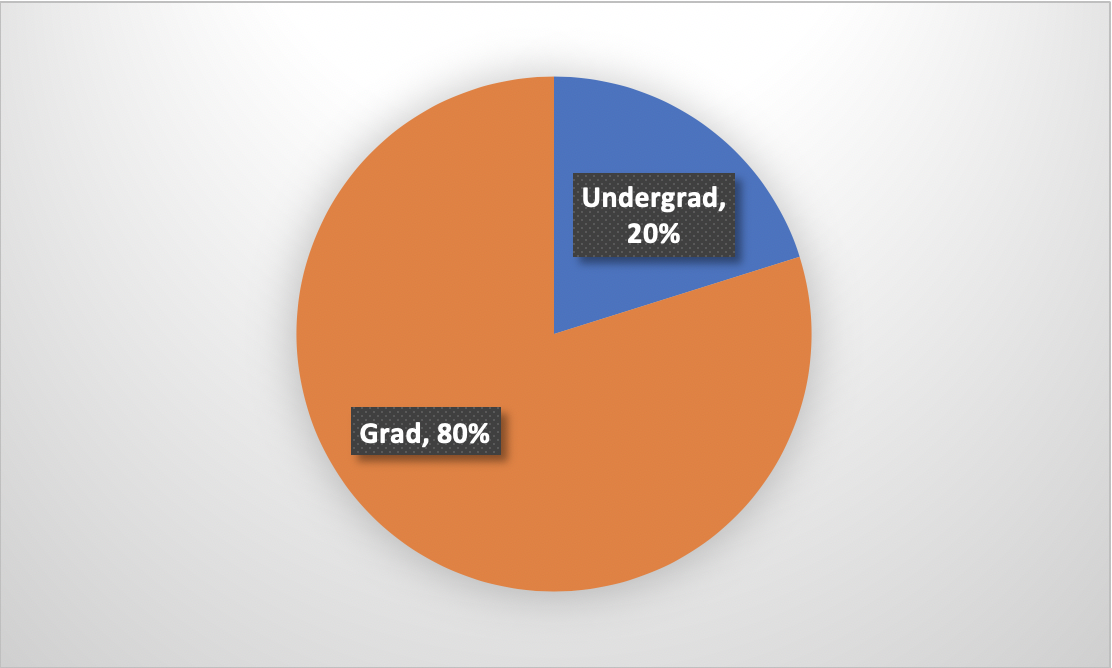

I started at Northern Arizona University in the fall 2007. I was 23 years old and a junior. Under the rules of the FAFSA, I was considered an independent student, but I didn’t qualify for any additional aid other than a few small scholarships due to having money in the bank from the house sale. I used that money to cash flow tuition, room, and board. Things were tight, but I didn’t take out student loans that year. (Justin and I started dating in March 2008.) For my senior year, I applied to be a resident assistant and got it! My room and board (and a small stipend) were covered that year. I didn’t quite have enough left to cover all of my tuition, so I took out two small student loans totaling $6,565. The small loan was subsidized, while the other was unsubsidized. (Subsidized loans do not accrue interest while you’re in school, but unsubsidized loans do.) I graduated with my bachelor’s in criminology and criminal justice in spring 2009.

Justin and I got married during the summer of 2009 and started our master’s programs that fall. From my earlier post:

During our grad programs, we were both graduate teaching assistants (GTA). Justin had a full-time GTA position for both years. While I had a half-time GTA position for the first year and a full-time GTA position for the second year. For reference, a full-time GTA position consisted of working 20 hours per week either grading for a professor and/or teaching a class. It also came with a 75% in-state tuition waiver, a $14k stipend for the academic year, and catastrophic health insurance. Our loans paid for the rest of our tuition, books, fees, and living expenses not covered by our stipends. We also saved some of the loan money for our eventual move as we knew we might be moving out-of-state for his new job and my Ph.D. program.

My part of our master’s debt was about $26k in unsubsidized graduate loans. Due to a combination of funding and Justin being employed, we didn’t take out any new student loans for my PhD. Since I was in school full-time and my loans were deferred, we focused on paying off Justin’s student loans first (about $20k). My final loan balance was about $42k after taking into account the interest that had accrued.

actually paying off the loans

So now you have a good idea of how much student loan debt I had and how I earned three degrees with relatively low debt. Now for the fun, and somewhat boring, stuff of paying it off. (Why is it that getting into debt always seems much more interesting than getting out of it?)

We had to start paying on the loans in October 2014, before I got a job, because my loans came out of deferment due to me dropping down to less than part-time status. When you’re in the dissertation phase you only pay for one credit per semester after you pay for the initial nine credits of dissertation. In order for the loans to remain deferred, I would have needed to be at least part-time (pay for 6 credits each semester) or jump through a bunch of hoops. My funding package covered all of my tuition except for the last three semesters of 1 credit each.

Since I didn’t have a job and it was the year of cancer (I promise a post is coming about that…), we decided to simply make the base payment of $472. We never looked into plans offering lower payments over a longer term because we could comfortably afford the standard 10-year repayment plan.

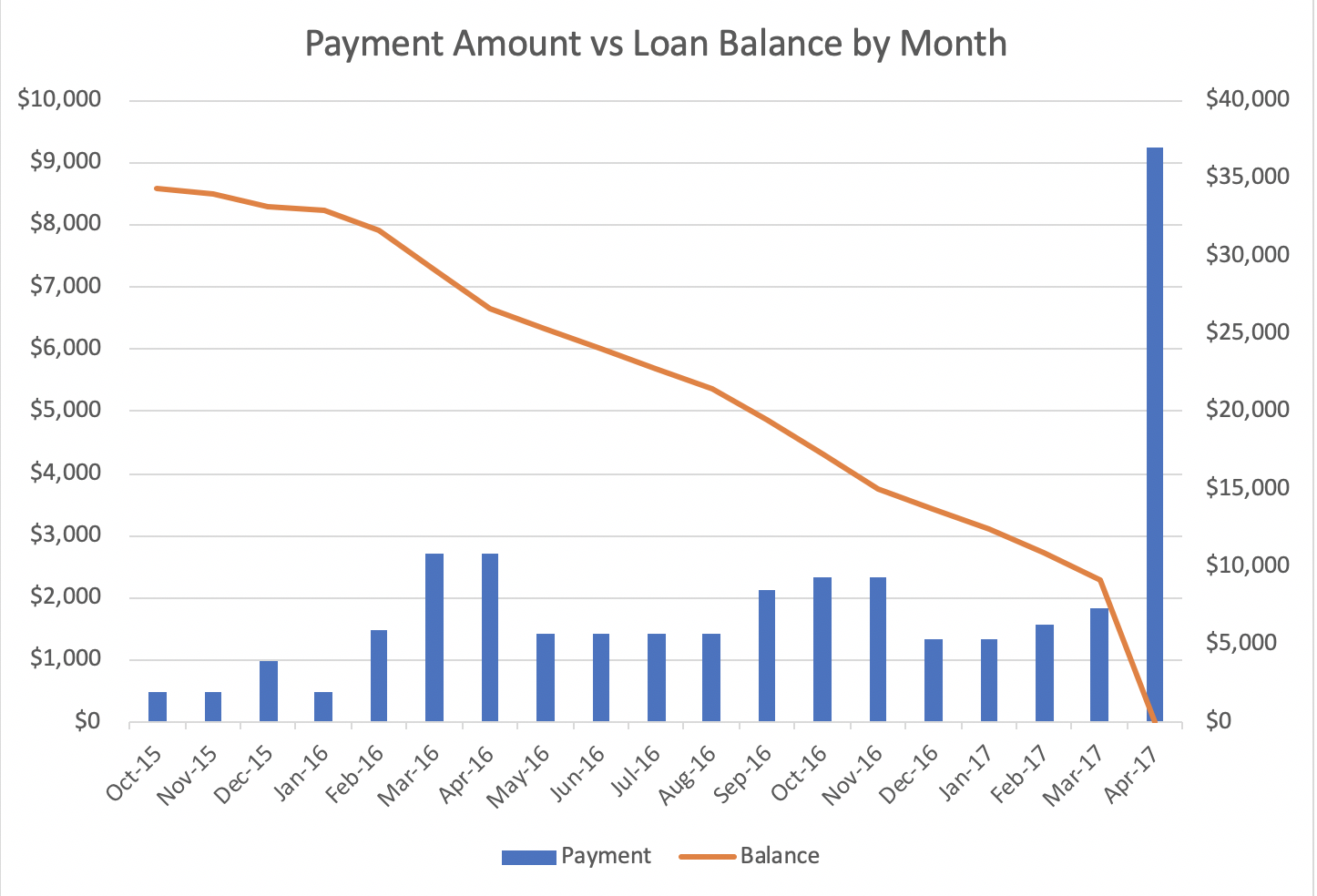

I started work in September 2015 and beginning in December we sent every additional dollar that came from my paycheck to paying down the student loans. Justin’s income covered all of our other living expenses. Essentially, we lived on half of our income.

There were a few reasons we waited until December to ramp up our debt paydown. First, I had surgery in August to remove my thyroid and we were waiting on all of the bills to come in. Second, and more importantly, we were paying on two mortgages. When I got the job, we decided to look for a home that would give us equal commutes. I was very ill, and it would have been impossible for me to drive 1.5 hours each way. We bought a home half-way in between but needed to float both mortgages until the tiny house (that I talked about in the previous post) sold. That house didn’t sell until late October. Basically, we wanted to wait until life had settled down a bit before going to town on the loans.

Once we started throwing everything we could at the loans, we sent an average of $2100 per month. My student loans were serviced by FedLoan servicing. While many people have had problems with them, I had a decent experience with them. My biggest issue was with how they handle payment processing. You can set up a direct debit for the amount owed on each loan (remember, I started with five loans) and add a fixed amount. We set up direct debits of the payment plus $1,000. It was actually frustrating because the maximumyou could add to the direct debit was $1,000 even though I wanted to add more. #firstworldproblems

However, the upside was that I could target which loan to pay towards first with the additional manual payments. Since all five loans were at similar interest rates (6.0-to 6.8%), I decided to tackle them in order of balance from lowest to highest. I really wanted an easy win to start the motivation – looking at you Dave Ramsey snowball. In September 2016, we paid off both of the undergraduate loans.

In April 2017, we used most of Justin’s bonus to finish paying off the remaining three loans. We usually have long talks about how to best use the bonus and usually opt to pay down a debt or put the money into savings. Importantly, we never bank on the bonus or the amount and treat it as extra money that fell in our laps.

the benefits of paying off the loans early

The first benefit, obviously, is no longer needing to make the payment every month. I think part of the reason that I didn’t have problems with FedLoan servicing is that I didn’t have to deal with them for very long.

I asked Justin to do a bit of analysis regarding how much we actually saved by paying of the loans 7.5 years early. By his calculations, we saved just over $15,000. This is HUGE. Imagine what you could do with an extra $15k in your pocket. That could be a new car, a down payment on a house, a fully funded emergency fund, etc.

We also became accustomed to living on Justin’s pay alone. This allowed us to take advantage of the fact that my (former) university offered access to both a 403b and a 457b. After the student loans were paid off, we immediately switched over to fully maxing out both of these tax-deferred accounts. It did result in a funny conversation with my HR lady about if I would be able to afford to eat, but totally worth it.

key takeaways or things you could do

- I don’t necessarily recommend taking a gap year in the way that I did but taking time to find stable (and somewhat flexible) employment helped to reduce the costs because I could completely cashflow community college and save for the four-year university. Also, since I was older when I went to the four-year university, I qualified as an independent student and had more financial aid available to me.

- Keep college expenses low. Going to community college and living with my mom for most of that time was the best thing that I could have done for keeping my overall college costs low. I graduated with my associate’s degree and all of my credits transferred to my four-year university.

- Don’t accept more loans than you need to cover expenses and decline unsubsidized loans first as they’ll accrue interest while you’re in school.

- Take advantage of jobs/work offered by the university. For all of my degrees, I was able to reduce costs by working for the school in one way or another. As a former professor, I can tell you that there are LOTS of jobs out there (many of them flexible) that students don’t often apply for. Take the money and make some solid connections while you’re doing it.

- Learn to live beneath your means – not just at your means. A big reason that we were able to go so hard on the student loans is that we were already used to living on Justin’s income. My income was “extra” money that could go towards other projects.

What have I missed? What do you still want to know?