Justin is a money nerd and I love him dearly for it. He has been tracking our net worth every month since the month we got married. Since we have almost 120 monthly money spreadsheets hanging out on the Google drive, I thought it would be fun to do a little bit of analysis. You know, because I’m a recovering academic and I can’t help myself sometimes. We like to joke that I know just enough statistics to get myself in trouble. Thankfully, this deep dive didn’t need me to call in the professional (aka Justin). All kidding aside, I was curious about what our lowest net worth ever was, when that happened, and when/how we managed to get to zero. If you read our monthly spending reports, then you know that we left zero and are in a very different place today.

Rather than focusing on where we are today, this post is about how we got here. Our story shows that you don’t need to make six figures to make significant life changes and grow your net worth.

how we got in debt and why I use net worth instead of debt figures

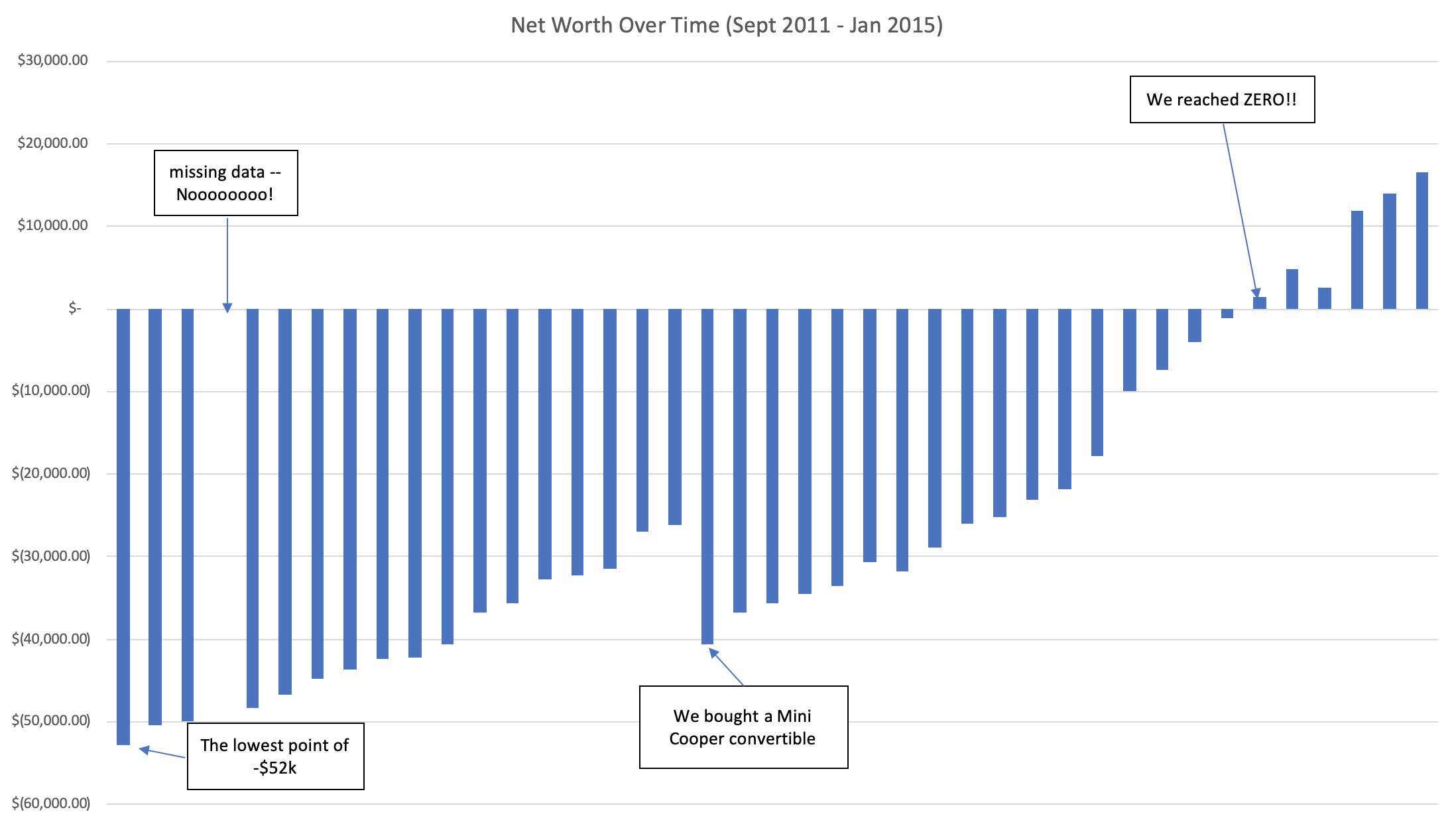

So, the first big question was: How low was our net worth at its lowest and when did this occur? Justin and I got married in 2009 before we started working on our master’s degrees. I knew that our lowest was most likely near then since we took on student loans to complete our degrees. It turns out that our lowest net worth was -$52,843 in September 2011.

Not surprisingly, the bulk of our debt was student loans and we owed about $56k. We acquired most of this debt during our master’s programs as our total student debt from undergraduate was about $10.7k. During our grad programs, we were both graduate teaching assistants (GTA). Justin had a full-time GTA position for both years. While I had a half-time GTA position for the first year and a full-time GTA position for the second year. For reference, a full-time GTA position consisted of working 20 hours per week either grading for a professor and/or teaching a class. It also came with a 75% in-state tuition waiver, a $14k stipend for the academic year, and catastrophic health insurance. Our loans paid for the rest of our tuition, books, fees, and living expenses not covered by our stipends. We also saved some of the loan money for our eventual move as we knew we might be moving out-of-state for his new job and my Ph.D. program. (Our plan was to pay back the difference if we didn’t move, but this kept us a bit more liquid.)

You might be wondering why I keep talking about net worth and not debt totals. Our goal has never been to pay off all of our debt. On the other hand, our goal hasn’t been to acquire more debt either. Rather, we see debt as a tool and neither as a negative or a positive. It is something we use to leverage our ability to achieve the larger goal of growing net worth. We define net worth as the difference between what you own and what you owe (Net Worth = Assets – Liabilities).

moving to Michigan

After graduating with our master’s degrees in May 2011, Justin and I moved to Michigan. We were fortunate to land a job for him and a Ph.D. program for me in the same state even though they were located in cities that were 1.5 hours apart. Due to timing, we found out about my acceptance to the Ph.D. program and rented an apartment (sight unseen) in Kalamazoo before Justin had his job offer. Thankfully, we decided to do a six-month lease because we ended up renting a second apartment in Lansing for Justin to live in Monday through Friday. It made for an interesting six months, to say the least.

As for our jobs, Justin was (and still is) an actuary and I was a sociology Ph.D. student. His starting wage was $50k. I had a full-time doctoral associate that covered 100% of my tuition and paid $17,500 per academic year. Justin’s job provided health insurance for both of us and books and paid the fees for my studies. As a result, I didn’t take out any new student loans for the doctoral program.

For the first six months, my stipend was enough to cover the Kalamazoo rent. While Justin’s pay covered all our other expenses. Back then, we didn’t have a car payment as our 2008 Chevy Aveo was owned outright. During the week, I had the car in Kalamazoo since I lived a bit too far away from campus to walk. Justin lived close enough to work to walk there (i.e., take the shoelace express). On Fridays, I would drive up to Lansing to get him and his laundry. Then we would spend the weekend together, and I would take him back on Sunday evening. At the end of our leases, we moved into an efficiency in Lansing. It reduced our rent a bit, though the tradeoff was a 1.5-hour commute (each way) to Kalamazoo two or three times per week.

increasing our net worth through wages and low spending

So now that you all have the lay of the land, how did we go about increasing our net worth? First off, our W2 wages (and let’s be real, Justin’s W2 wages) steadily increased from the start. In 2011, we grossed $46k. That year our pay included one semester of our full-time GTA jobs, six months of full-time employment for him, and one semester of doctoral associateship for me. In 2012, we grossed $58k. In 2013, we grossed $76k. In 2014, we grossed $91k. I wasn’t employed for the second half of the year because my associateship was limited to three academic years. Justin’s yearly increases in pay came from merit increases, promotions, raises for passing exams, and annual bonuses. Essentially, Justin is really good at what he does.

Growing our income was only part of the equation. We also kept our expenses low by only owning one vehicle, living in small, affordable spaces, and not traveling. We did trade-in the Aveo for a Mini Cooper in 2013 (Justin’s quarter-life crisis). We ended up financing the car at a very low-interest rate. While it was a hit to our net worth (Justin doesn’t include vehicles in the assets section, only in the liabilities section), we loved every second of owning that car. (By the way, she’s still in the family. We gifted her to Justin’s mom when we decided to downsize to one car again, but that’s a story for another day.) We also bought a house in 2013. It was a two-bedroom, one-bathroom home that we got for $44k. You read that right. We bought a home for less than $50k. Our mortgage ended up being less than half of our apartment rent. Between 2011 and 2014, we only took one big trip and that was to Texas for my brother’s wedding. All our other trips were either for work or inexpensive weekend trips.

In many ways, we were too busy working on our careers to notice that we were making big moves in our finances. For the first five years of Justin’s employment, he worked on the actuarial credentialing process that consists of taking exams every six months. Each exam required 300 to 400 hours of study that he had to do mostly outside of working hours. In addition to taking three classes, I taught one of my own each semester, volunteered, and did my own research. We didn’t see very much of each other during those years.

Not having time and putting most of our finances on autopilot made things go a bit faster. From the time Justin started working, we contributed to his 401k to get the match from his employer. Any money that wasn’t needed for paying bills was put towards his student loans. We didn’t work much on my loans at the first because, since I was in school full-time, they were in deferment and not accruing interest (mostly). A goal of ours was to have his loans paid off before mine became due.

We reached a net worth of zero in August 2014, just shy of three years after we hit our lowest net worth. In full disclosure, we weren’t debt free. We still had a mortgage, a car loan, and my student loans. The point is that our assets were finally worth as much as our debts. We didn’t really do anything all that special to get there. It was the combination of growing our income through employment, keeping our monthly expenses low, and contributing to our tax-deferred accounts. We had some splurges along the way (e.g. the convertible), but also made sacrifices like taking ‘staycations’ when we would rather have been traveling. For us, it was about having a shared vision and supporting each other as we made that a reality.

I love looking at debt as a tool. I think the overarching message of “debt is evil” is really limiting – maybe that’s just because I have a lot of debt, though. 🙂

LikeLiked by 1 person

I have very complicated thoughts about debt on both the individual and societal levels. (I may have to write a whole post about this!) For individuals, debt can either work in their favor or not. It comes down to the intentionality or the reason behind the debt. I’ll give an example. My brother and I both bought new cars within a month of each other for similar prices. We both took out loans, but this is where things get messy. His loan was at a staggering 18% for 6 years, while my loan was at .09% for 4 years. Clearly, I had more favorable terms. Was his debt bad? Well, it certainly wasn’t great. He was convinced (for a lot of reasons) that he needed a new car. I even told him that he should consider a used car and he would have avoided most, it not all, of the debt. He’s more financially “woke” now and is working furiously to pay his loan off. Meanwhile, I’m just letting our loan do it’s thing because I just don’t see the point of paying it off early. Debt becomes “evil” when forces outside of the individual (cultural, societal, etc) encourage it. When the idea of debt is the norm and the ideas frugality are weird — the inversion of values — we have bigger problems than if someone should buy a latte or not. Like I said, complicated thoughts that I probably need to organize better. 🙂

LikeLike

I think we probably have similar ideas about it. Nothing is black and white…for me, especially, I am surprised that so few people see it as the gift that it can be (not like “here’s $10K in debt, go crazy,” but like “wow I’m lucky to have access to that). My in-laws live in Ukraine and they just don’t have access to the credit we do. So when the car breaks, you lose your job. Or if your teeth fall out, you endure excruciating pain until you can scrape money together. Debt can be crushing and it can be awful, but it can also be life-changing.

LikeLike

Lack of perspective is definitely an issue that I see. We live in a world where people can finance things like lunch and see using credit as trivial. Whereas in other places, micro-lending is a thing that allows people to buy one goat or one sheep and it totally changes their life. It’s part of the reason that I see debt as a tool, but just like a hammer isn’t always what you need to get the job done, neither is a credit card. There is a time and a place for it.

LikeLike