I know it’s been a bit since I’ve written. I wish I could say that I’ve taken a long break because I was doing something cool, but I was just living life and doing my best to keep everything together as a stay-at-home mom to a disabled child during a pandemic. Yeah, I haven’t been busy in the slightest.

We did manage to make one of our financial goals happen though — we had the private mortgage insurance (PMI) removed from our loan in November 2021. Since many people don’t know much about PMI, I thought I would talk a bit today about the process we went through to have it removed.

Before I dive in, a little background:

We bought our townhouse in August 2019 — yes, the same month we were matched with LP — for $460,000. Based on the math, we decided that it would be cheaper for us to pay the PMI and only put 5% down instead of accessing the money we have in savings for the full 20% down to avoid PMI. (A lot of folks will tell you to avoid PMI at all costs, but we say DO THE MATH!)

Our big goals were to have the PMI removed in three years and to payoff the house in ten years.

According to our loan documents — and this is common language — there are two scenarios that should trigger the removal of PMI.

- You pay the loan balance down to less than 78% loan-to-value (LTV) where the value is the value of the home used in the loan; or

- Your home appraises sufficiently enough in value to bring the LTV to less than 78%. Typically, you would be responsible for paying for the appraisal showing this value increase.

Essentially, you need to either decrease the numerator or increase the denominator in the LTV calculation. (LTV = (Mortgage balance/ Home Value) * 100))

While lenders prefer the first option because it tends to be more conservative, homeowners typically try for option two because for many it’s much more likely that the home will increase in value faster than the principal will be reduced. Knowing our financial situation and our big goal of wanting to pay the house off in ten years, we knew that option 1 would be the most prudent course of action for us.

Our path to 78% LTV is a little convoluted, so bear with me.

With our aggressive payoff plan, we pay a significant amount towards principal every month. When we took out the 30-year mortgage, we were paying an extra $538.19 per month to principal which made our total monthly mortgage payment $3100. Eventually, we were able to increase our additional payments to principal to make our mortgage payment total $3600 per month. We also send a significant portion of Justin’s annual bonus to the mortgage. By the time we had decided to refinance the house, we were already halfway to having the PMI removed. Essentially, this approach had us purely attacking the numerator part of the LTV equation.

When mortgage rates were first on the decline in 2020, we decided to refinance the house into a 15-year term with a lower interest rate. Refinancing the house triggered the need for a new appraisal, which due to a miscommunication by our broker ended up being paid for by the bank. It was a happy mistake for us. The new appraisal showed that our home had increased in value to $486,000 — increasing the denominator. Prior to the new appraisal, we were 53.4% towards having the PMI removed. After the appraisal, we were 75.2% towards having the PMI removed. It was a huge improvement. So, refinancing benefitted us by showing our LTV was lower and getting us closer to our first goal.

The second benefit of refinancing was that our monthly PMI payments were cut in half. On the 30-year term, our monthly PMI payment was $91.04. When we switched to the 15-year term, our monthly PMI payment was reduced to $48.10.

After the refinance from the 30-year to 15-year term, our mortgage payment did increase, but not above the $3600 that we were already paying monthly. For the first few months, we continued paying that but were able to increase it to its *final* amount of $3800 last April. (I say final amount because we don’t have to make any more changes in order to reach our 10-year payoff goal.)

Using the appraised value from the refinance, our mortgage hit the required balance to meet 78% LTV in July 2021.

Did our lender automatically remove the PMI? Heck no! That would make this story entirely too simple.

We decided to give the bank some grace and didn’t call about the PMI being removed until September. We had a lot going on with visitors during the summer and this task just stayed on our never-ending to-do list.

When Justin called to have it removed, the representative said that they would mail us some forms that needed to be filled out to get the process started. Super annoying, but whatever.

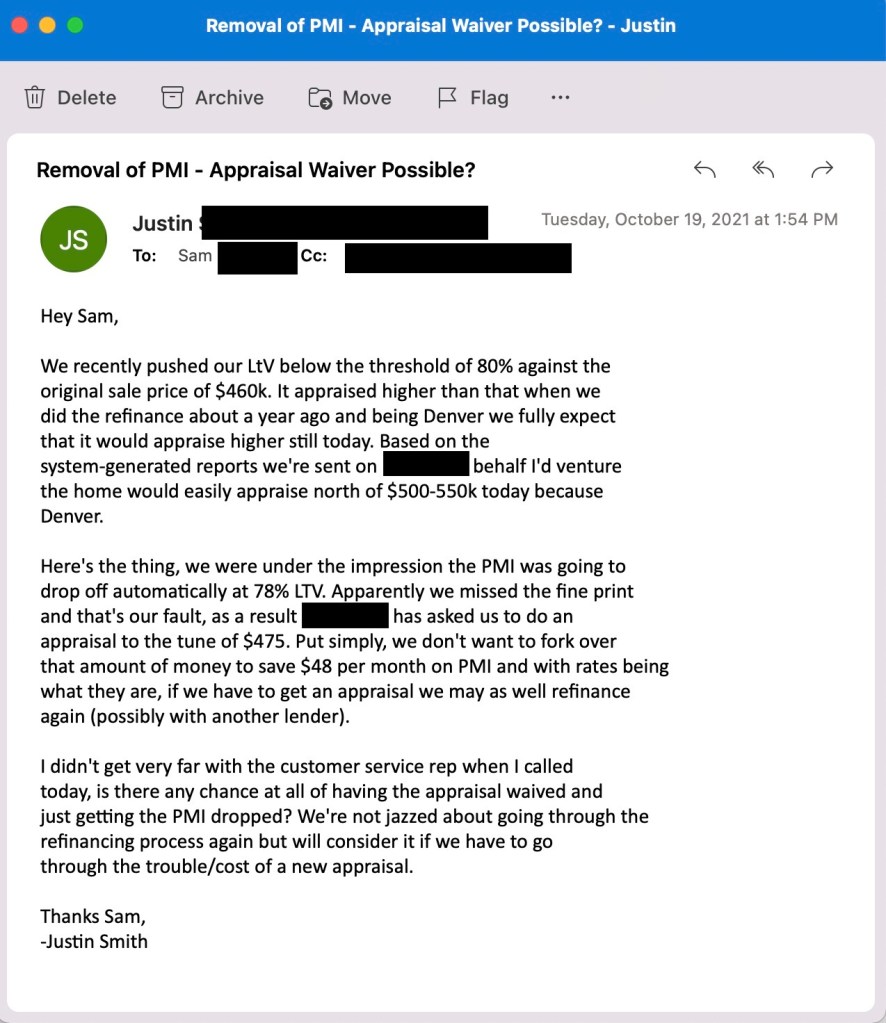

The forms eventually arrived, but they weren’t really “forms.” Instead it was a document explaining that we would need to pay for a new appraisal to be completed to show the value of our home had increase sufficiently to lower our LTV. The document implied that PMI removal was unlikely to happen. The cost of the appraisal would have been $475 (aka 10 months of PMI payments). No where did the document mention anything about the loan balance.

I told Justin that we weren’t paying for an appraisal and to call them back. This time he explained in detail why our PMI should be removed based on the fact that our loan balance was now less and that, not the increased value, put us below the required 78% LTV. He explained that having another appraisal made no sense and that we had contractually fulfilled the requirements. The representative wouldn’t budge.

At this point, we had a couple of options. We could try to argue up the chain of command at the bank or, since we would have an appraisal anyway, we could refinance again.

Then it dawned on me that we should email our mortgage broker at the bank. He had shown us over time that he was willing to think outside the box. We knew he couldn’t approve removing the PMI without an appraisal on his own, but that he would know exactly who to contact to make it happen.

And so he did. Those emails are below.

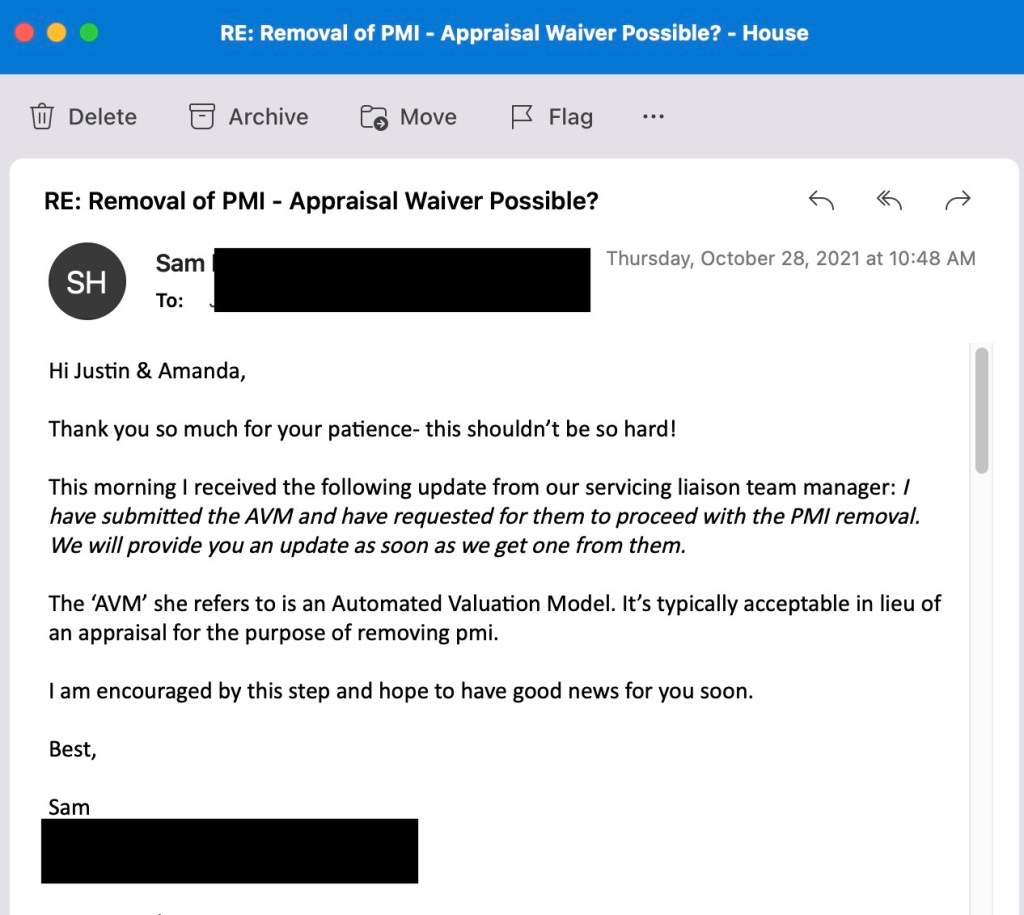

Thankfully, Sam (the mortgage broker) was completely on our side and just as annoyed as we were by the end. It took about six weeks to get it done. However, he did manage to get it done without us paying for a new appraisal!

Working hard to have the PMI removed saved us thousands of dollars. Looking at our original amortization table for the 30-year term, we would have made 103 PMI payments if we paid the loan as written without our extra principal payments. That’s money that would have never benefited us.

Even refinancing to the 15-year loan helped to save us money on the PMI. At the end of it all, we only paid 53% of the total PMI that we thought we would pay at most.

| PMI Amounts | Difference (i.e., SAVINGS) | |

| Projected for original 30-year term | $9377.12 | $7621.56 |

| Projected for 3-year goal | $3277.44 | $1521.88 |

| Actual paid | $1755.56 |

To really bring it home, DO THE MATH. Sure, having to go through the process and annoyance of getting the PMI removed was frustrating. But, if you’ll remember why we decided to put less than 20% down in the first place, it was more cost effective for us to have PMI than to access the money we did have.

Nothing major happened after the PMI was removed. There wasn’t a parade or balloons. Instead, I simply adjusted our extra payment to principal to keep our monthly mortgage payment at $3800.

On to the next goal!