Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time. Every month, I report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often see general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income.

I use Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

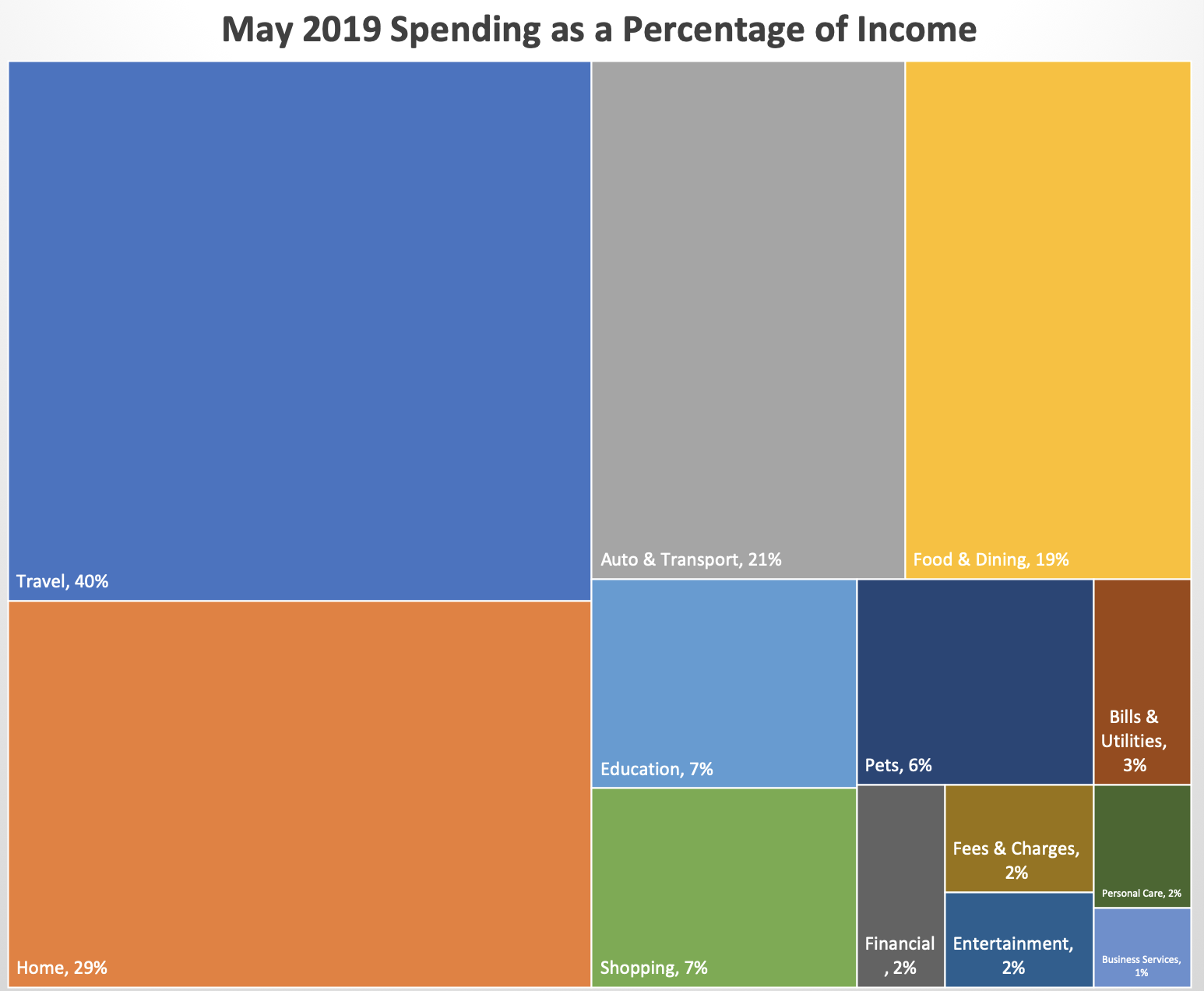

Without further ado, here’s where we ended up at the end of May 2019.

travel expenses

Well, it finally happened. Our top three expenses do not include food expenses. Although, I’m still going to talk about food any way since I always talk about food.

Travel expenses made up 30 percent of our spending and 40 percent of our income. It was a big month for us. We bought the plane tickets for our South Africa trip in August, put the deposit down for my yoga retreat in Bali in October, and paid my global entry application fee.

Since we don’t know when we’ll be matched with an expectant mom, we’ve decided to do as much travelling this year as humanly possible. Of course, lots of travel comes with expenses. As far as we’re concerned, expenses are really not a problem as long as you plan for them. You may recall that a big part of our 2019 goals was to travel. We cut back in other ways, primarily our savings rate, because of the trips we wanted to take. While we both very much want to be FI, we also want to have fun and enjoy our life now. It’s all about the balance.

We bought the South Africa tickets through the Chase portal. This allowed us to use our accumulated points towards the cost of the tickets and got the price down by about a third. There are also the added benefits of being able to cancel the trip for a nominal fee (if something awesome happens, like a baby!) and that they’ll take care of us if our trip gets disrupted for some reason (like the time there was a blizzard in Ireland and we got stuck in Spain). I got into the travel hacking about two years ago and so far, we’ve done well. (SN: DO NOT travel hack unless you pay off your credit card every month!).

One of my favorite yoga teachers and friends is hosting a yoga retreat in Bali, Indonesia for a week in October. We paid the deposit this month and will be paying for the rest of the retreat in July. I’ll also need to buy my plane tickets, but I may try to travel hack it. United is often running a 60k point bonus. However, I have to wait until we close on the house since the mortgage folks frown upon new lines of credit. It will be easy to meet the minimum spend for the bonus though since we’ll need appliances for the house. (Win-win in my book).

Finally, we both decided to apply for global entry since we have a fair amount of international travel this year. Justin applied for his in April and I got around to doing my application in May. Global entry is like TSA Precheck plus. Essentially, you get all of the perks of TSA Precheck and get expedited reentry to the United States when coming home from trips. It’s good for five years and since both of us have it, our child also benefits.

home expenses

Home expenses made up 21 percent of our spending and 29 percent of our income. In addition to rent, we bought some stuff for our home. I decided that we needed a strawberry planter, strawberry plants to fill it, and some adorable succulents. Justin and my brother LOVE strawberries, so it seemed like a good idea to try my hand at growing them. Our subscription of dishwasher pods also came in this month.

The new house is chugging along. We had our pre-insulation meeting during the second week of May. Basically, it was our last time to add anything (like an extra outlet in Justin’s office) before they installed the drywall. We also passed our first set of inspections. Things are looking good and they are still aiming for an August completion date.

transportation expenses

Transportation expenses made up 15 percent of our spending and 21 of our income. It was an abnormally expensive month for us as we had the car payment, car insurance premiums, and car registration due.

We pay six months of car insurance at once. This time, we got a rather pleasant surprise. Our premiums actually decreased by $30. That’s pretty much a tank of gas and two lattes, so I’ll take it! I just learned about pay-per-mile car insurance, but it’s not in Colorado yet. I’ll definitely be taking a look though when it becomes available here. Since moving, we maybedrive 200 miles per month – a significant decrease from when I was commuting 90 miles roundtrip to campus. It would be nice if we could get our insurance premiums even lower.

We’re still on track to have the car paid off by October 2020. This is actually six months sooner than the loan actually calls for since we pay a little extra every month because Justin and I like nice round numbers. (We rounded our payment up to the nearest $100.) We keep going back and forth on whether we should pay it off early or not. On the one hand, the interest rate is super low and having the loan doesn’t bother us. We have the money in savings, but it’s currently earning at a much higher rate than the loan’s APR. On the other hand, paying it off would free up some monthly cash flow for other things. With the upcoming home closing, we’re trying to stay as liquid as possible so this is probably a moot point.

food costs

Food expenses made up 14 percent of our spending and 19 percent of our income.

Even though we aren’t quite where I want us to be yet, we did okay this month. First, we didn’t buy any meat from the grocery store. All of our meat came from our previous month’s locavore delivery. Otherwise, we ate vegetarian meals or had meat when we ate out.

We were doing really well until the last week of the month. We’re going on a trip and I like to leave with the fridge as empty as possible. This worked a bit too well as I achieved the goal of the maximum fridge emptiness a few days earlier than planned. We decided to order in for a few more meals than normal and erased all of our awesome work. On the upside, we didn’t go backwards in that we’re still on par with our 12-month average and this wasn’t our highest month of the year.

I’m already mentally preparing for June though. The first part of the month we’ll both be travelling, and later I’ll be in Michigan for a week. This means that there’s going to be a lot of eating out. Some it will be reimbursed by Justin’s employer, but certainly not all of it.

the actual percentages

Below are the rest of the month’s spending percentages.

Our pets spending remains higher than usual, but I think we’ll be back to normal starting next month. I recently wrote about our pet spending over time. It was quite eye-opening!

Education was also a bit higher than normal. Justin is taking a couple of classes at our local community college. As an actuary, he works with accountants quite a bit and learning more about what they do will help him out in the long run. His employer reimbursed us for the tuition, but we still needed to pay for his textbooks. He also took a one-credit class on welding safety since that’s a hobby he has an interest in.

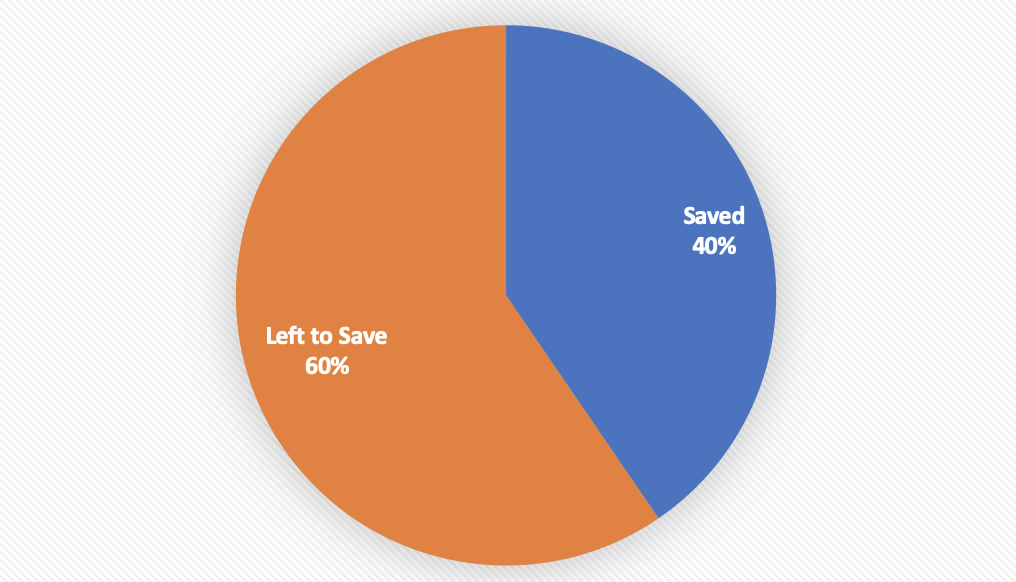

progress to fi

As of this month, we are 40 percent of the way to our fi number. Despite the dips in the stock market this is the same as last month because I found out that I wasn’t including the balance of Justin’s other retirement account with the Colorado company. It was sort of like finding $20 in your winter coat pocket!

How did your month go? Were you able to achieve your financial goals?

This is so great! I also am paying off my car payment early, also because I like round numbers, but…the payment is $396 and I pay $400, so it’s not going to take much off! Our mortgage is the same way, though, and I end up paying about 7% extra every month (that will end up about 15% extra every month), which pays off over a 30-year mortgage!

LikeLiked by 1 person

I’m glad I’m not the only one who likes round numbers! Every little bit helps though and it makes keeping my checking account nicer. (If only everything were so simple.) I’ll have a post about our house payoff plans after we close in the fall. Spoiler warning: Justin wants to pay it off in *eight* years! It’s doable, but definitely a challenge. More to come though!

LikeLiked by 1 person