Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time. Every month, I report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often see general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income.

I use Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

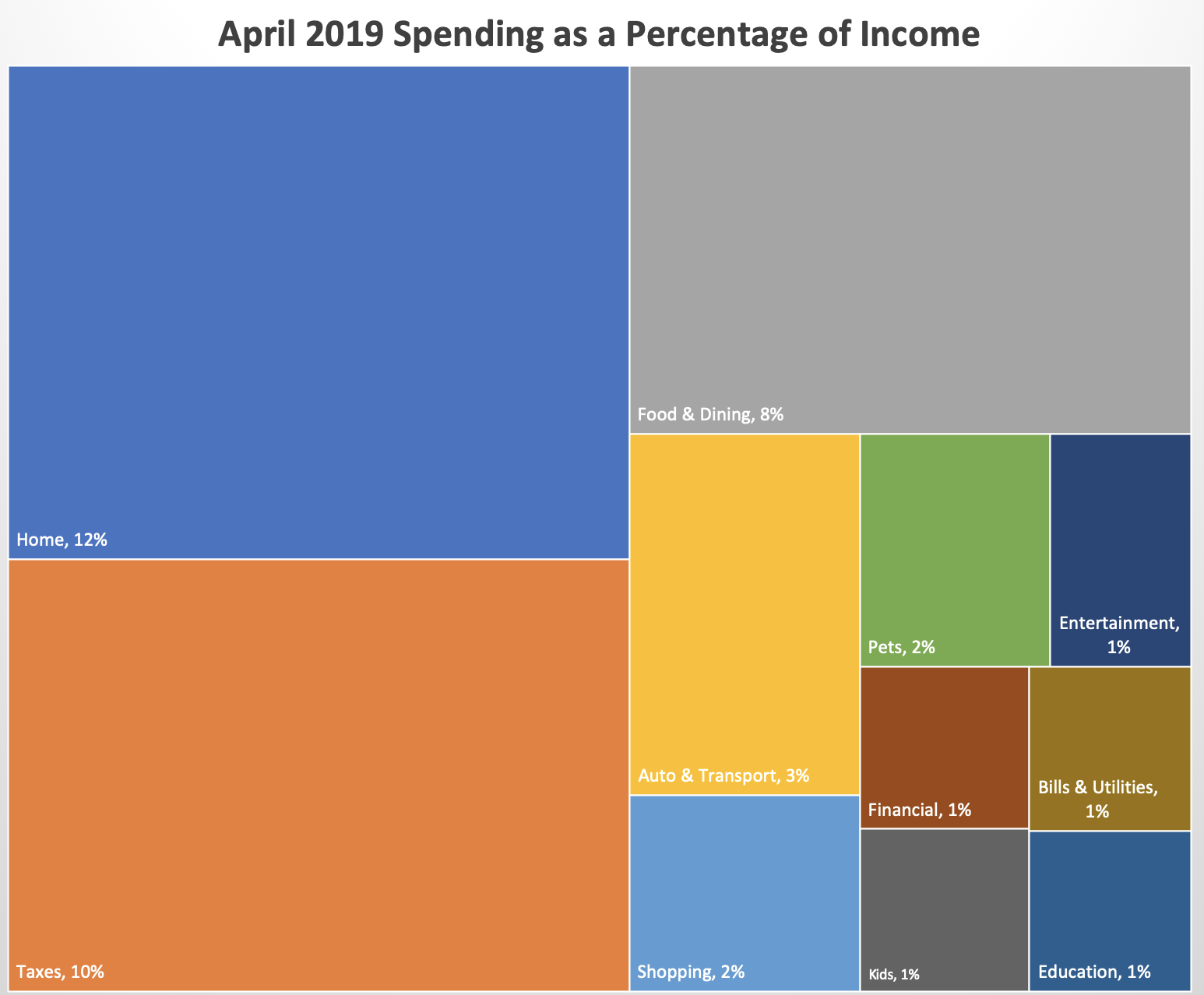

Without further ado, here’s where we ended up at the end of April 2019.

taxes and uncle sam

Well, Tax Day sort of sucked. We ended up owing a fair amount to the federal government and got minor refunds from the rest of our taxing entities. Taxes and preparation software (i.e., TurboTax) made up 25 percent of our spending and 10 of our income. I purposefully waited for Justin’s annual bonus to come in so that tax time wouldn’t hurt as much. I’ve known we would owe for a few months and wanted to smooth things out.

Because we live in one state and have jobs in a different state, our taxes were slightly more complicated than usual. We had to file taxes with *five* different places: the feds, two states, and two cities. Our taxes looked like an arts and crafts project. Thankfully, next year will be simpler because we’ll have lived in one state for the entire year. I won’t have to figure out where we lived for each transaction and pro-rate accordingly. Also, 2019’s taxes are the last time that I’ll need to file in the city of my former employer. Less paperwork is a win in my book.

Owing taxes blows, but it’s the right problem to have. I did a comparison between the 2017 and 2018 numbers. While we made more money this year and, consequently, paid more in taxes, our overall tax rate was actually lower. 2019’s taxes will be interesting since we’ll make less money this year with me leaving my job and we’ll be able to claim the adoption tax credit. (We couldn’t claim the credit this year because we don’t have a finalized adoption and we paid the money this year.)

housing

April was a typical housing expense month for us. Housing was 28 percent of our spending and 12 of our monthly income. We had our typical housing expenses this month of rent and home supplies (like new dish scrubbers). We also paid our annual renter’s insurance premium. Now, some of this is likely to be refunded after we move to the new house and are no longer renters.

By the way, this is totally an insurance coverage you should have if you rent. Your landlord is only responsible for the building if something happens. Our last apartment in Michigan flooded during a construction mishap. While the landlord handled getting the apartment fixed, it was our renter’s insurance that covered getting our damaged belongings replaced. Thankfully, we’re fairly minimal people and didn’t have that much damage, but it could have been a lot worse. Okay, I’ll get off my soapbox now!

In other news, our new house has been framed! The next steps are for the HVAC system, electrical, and plumbing to be installed. It’s very exciting.

food costs

Food expenses made up 19 percent of our spending and 8 percent of our income. We did not do well this month in controlling our food spending. I’m actually a bit disappointed in us. This month we spent about $200 more than our 12-month average, effectively erasing the gains of the last two months.

We went over in two of the three food categories that I track: groceries, restaurants, and alcohol & bars. For groceries, we had some friends out at the beginning of the month and cooked at our place a few times. We did chicken and steak fajitas and I know that the cost of meat alone for that meal ate up a sizeable part of the overage. As of this writing, we haven’t had the refund from the jar debacle processed yet. Between the two of these, I know what happened to the grocery budget. Similarly, we ordered pizza when they were here from our favorite pizza place. While incredibly tasty, it was also spendy. Would I do it again? Most definitely!

For the most part, we met our goal of only eating meat that was in our delivery. The big exception was the previously mentioned fajita night. We didn’t have enough on hand to feed six people. We were going to do a lobster mac-n-cheese night (one of my guilty pleasures on so many levels: lobster (yum!) and vegan mac-n-cheese (double yum!)), but, after seeing where we were at budget-wise near the end of the month, we decided to skip it.

We’ve already made May’s monthly menu. We’re sticking to delivered meat only again and we’re working on cleaning out the freezer because it’s a little out of control. Towards the end of the month, we’re having a fridge/pantry cleanout since we’ll be gone for a week.

the actual percentages

Below are the rest of the month’s spending percentages. With the exception of the pets category, everything was fairly typical. I suspect that the pets budget will need to be revised in light of Scooter’s ongoing medication needs.

Justin was paid his annual bonus this month. That’s why the percentages seem a bit lower than usual.

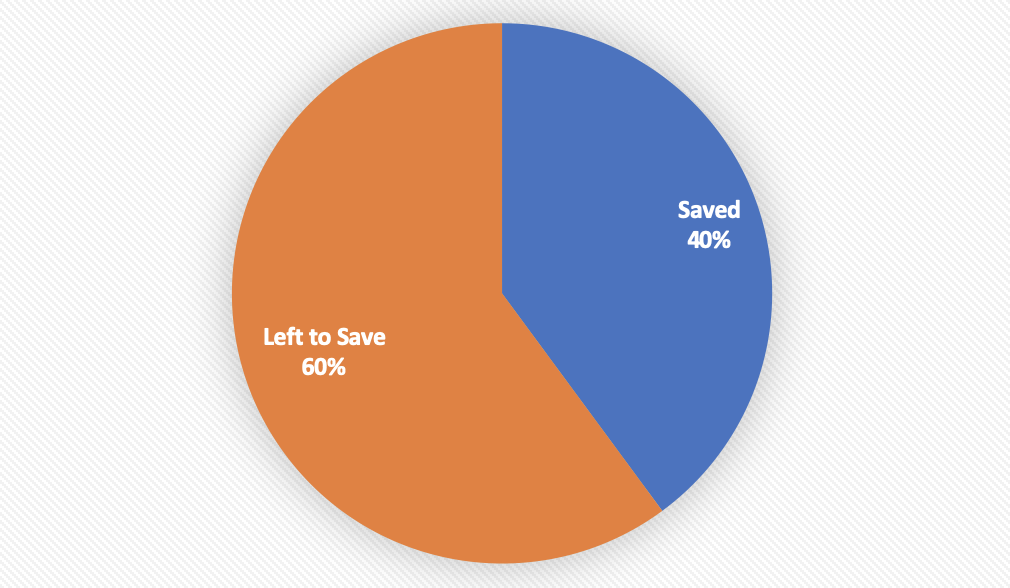

progress to fi

As of this month, we are 40 percent of the way to our fi number. This is a 4 percent (!) increase over last month. We put the majority of Justin’s bonus into savings as we’re planning on closing on the house later on this summer and new houses come with new house expenses (like appliances). I report our numbers as they are currently with full knowledge that it’ll likely decrease later.

How did your month go? Were you able to achieve your financial goals?

Thanks for sharing. Love the visuals

LikeLike

Thanks! I’m a bit of a data visualization junkie!

LikeLike