Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time and now feels like the time that increased accountability through reporting our monthly finances. Every month, I’ll report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income. In addition, I’m not quite ready to discuss our actual numbers as I think that both detracts from what we’re trying to do and I want our story to be a bit more approachable.

I used Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.” Without further ado, here’s where we ended up at the end of February 2020.

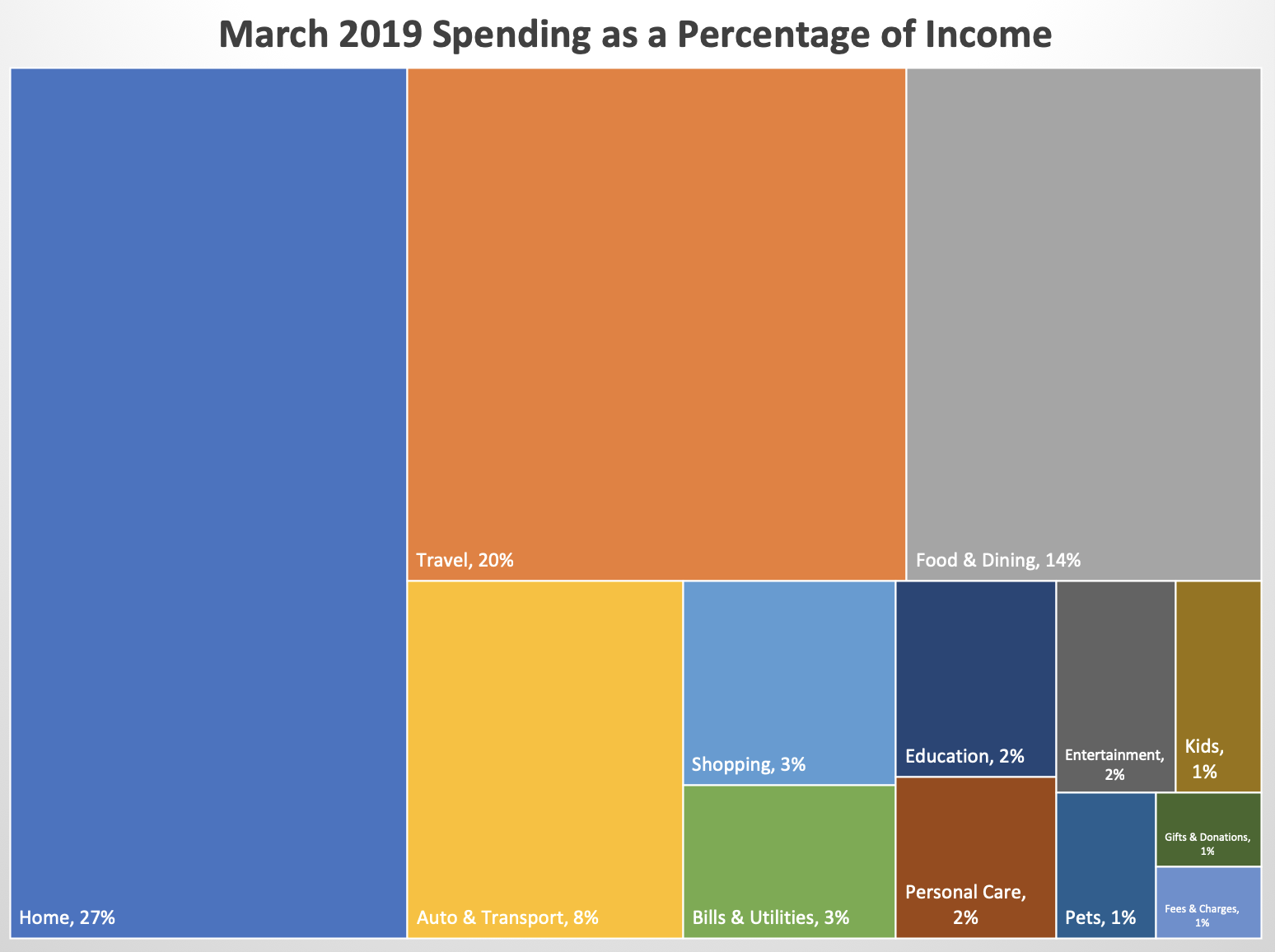

home expenses

March was a pretty typical month for us. Home expenses made up 33 percent of our spending and 27 percent of our income for the month. This category includes rent and home supplies.

In other news, more progress has been made on the new house. They started framing this month and we already have a first floor! It’s super neat watching the house come together and I love that the builder sends us regular updates and photos.

travel expenses

Travel was our second highest category this month. It made up 24 percent of our spending and 20 percent of our income. We bought the plane tickets for our Bermuda trip and got our vaccines for South Africa. We’ll be reimbursed for half of the plane tickets by Justin’s work since the primary purpose of his trip is a conference.

Traveling out of the country calls for double checking that you have the appropriate vaccines. We were referred to a travel clinic by our primary care doctor since they have all of the information about exactly which vaccines are needed for which countries. We both had to get vaccines for hepatitis A and typhoid. While were gone, we’ll be taking malaria prevention. It was neat and little scary to learn about all of the possible hazards of our trip. When the nurse practioner showed us the map of the world, the United States is largely blank for most illnesses. Every where else had one or more illnesses/dangers for us to be aware of.

food expenses

As usual, food expenses made it into our top three spending categories for the month. In March, food expenses made up 17 percent of our spending and 14 percent of our income.

We did pretty good this month. This was our lowest food expense month of 2019 thus far and about $300 less than our 12-month average. In April, we’re focusing on only eating meat that comes in our Locavore delivery. Otherwise, we’ll be eating vegatarian meals and cleaning out the freezer. I’m looking forward to seeing how April turns out!

the actual percentages

Do you ever look at the craziness of one month and think, “next month has to be better” orthink, “at least we stayed under budget”? That’s where we’re at this month. That huge hit from travel sort of shocked me. I knew it was coming, but seeing the large orange square put it into perspective.

We did have a frugal fail this month. Every month, we pay the full statement balance to the credit card in order to avoid paying any interest. I must have gotten my dates mixed up or something because I paid it two days after the statement balance was due. Ugh! Live and learn, I guess.

fi progress

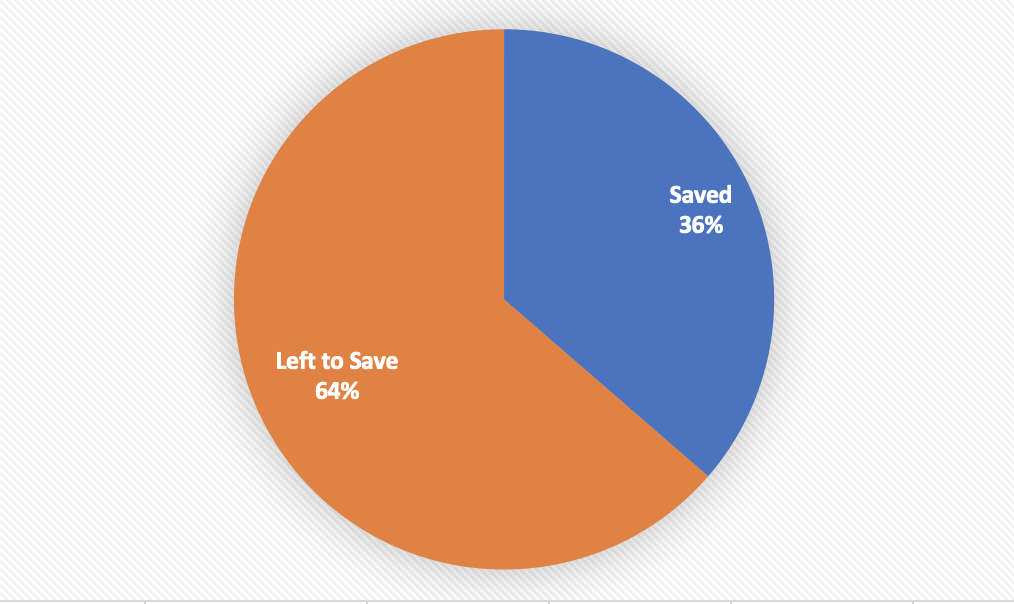

We hit all of our savings goals this month. Woot!

Every month, in addition to the tax-deferred savings that doesn’t come to our checking account, we save about 35 percent of our income. Most of it goes to our regular savings account, as we’re trying to stay a bit more liquid than usual with the house purchase, a portion of it goes to our brokerage account, and a small portion goes to college savings (that’s the 2% education spending above that doesn’t get counted in our fi number).

I’m leaving my job at the end of May and June will be my last paycheck. That will mean a reduction in our savings starting in July as we currently put my entire paycheck into tax-deferred accounts. I’m planning on doing some calculations about where this change and the home purchase will put us fi-wise later in the fall. Until then, we’ll keep doing what we’re doing.

How did your month go? Did you meet your goals?