Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time and now feels like the time that increased accountability through reporting our monthly finances. Every month, I’ll report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

This is our first spending report since August. There are some good reasons for the delay. First off, my semester has been a bit wild and by the end of September I was in the weeds and our blog had to go on the backburner. Don’t worry, I’m back. The semester is winding down and next semester is already set up and ready to go. Who knew that teaching two online classes from scratch would take so much work and time!? Secondly, we’ve had some employment shake-ups that have caused things to be a bit nuts with the numbers. More about that below. Finally, we’re ready to share what our special project has been and that has also wreaked havoc on the numbers. Basically, the perfect storm of no time and stranger than normal finances caused me to put the report aside.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income. In addition, I’m not quite ready to discuss our actual numbers as I think that both detracts from what we’re trying to do and I want our story to be a bit more approachable.

I created the report a little bit differently this month and I think I’m going to stick with it for now. Previously, I was pulling from our pay stubs. However, that became a bit more complicated than I would have liked over the past few months. Instead, I used Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

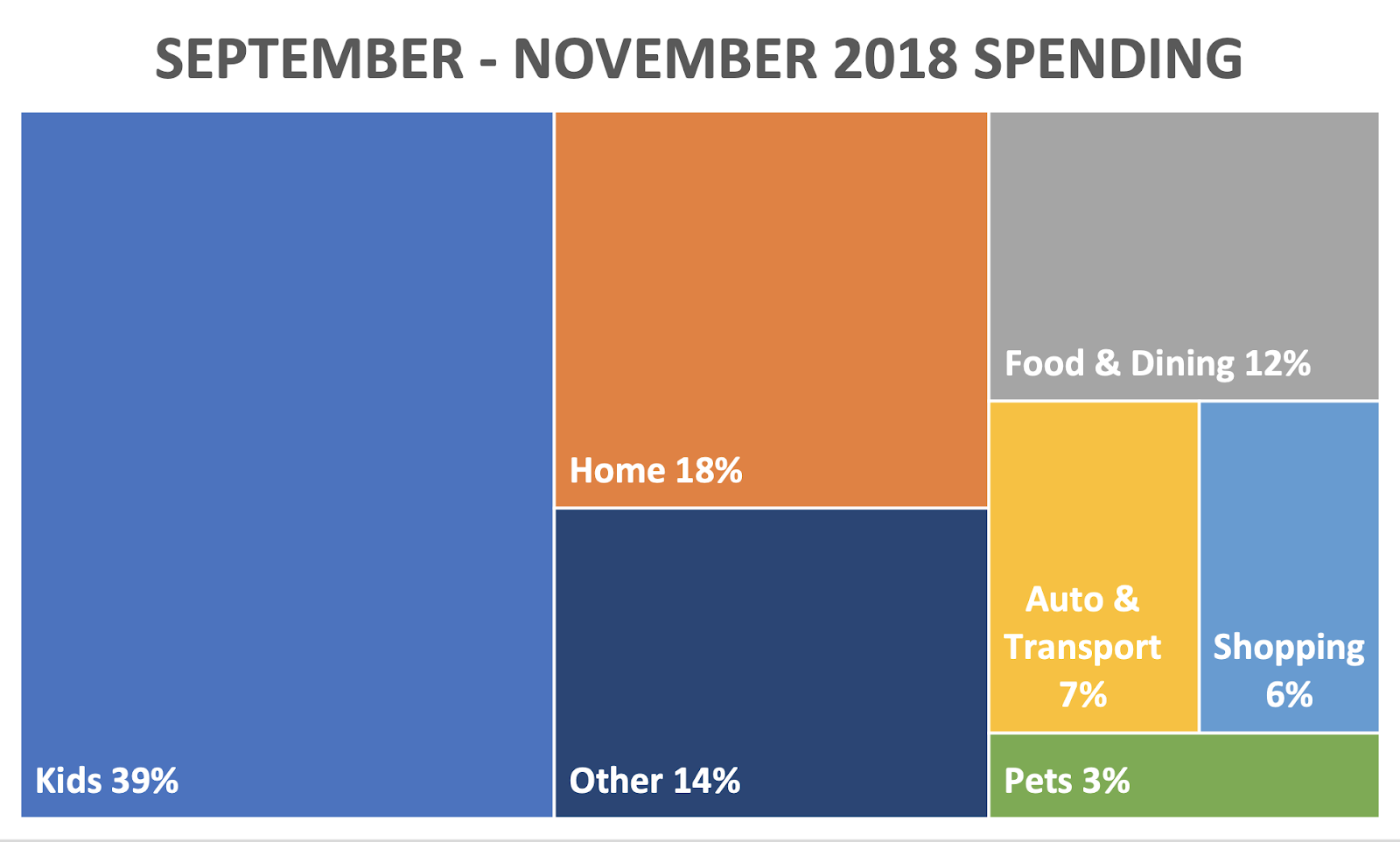

Without further ado, here’s where we ended up at the end of November 2018 with numbers for September and October included.

A special project is in the works

We’re finally reading to reveal our special project that we’ve been working on over the past few months. Mr. Smith and I have decided to expand our family with a child through adoption. It took several months, but we have completed our home study! In other words, the State of Colorado has found us fit to parent. At this point, we’re in the pool and waiting to be chosen by an expectant mom. To be clear… the waiting could take a LONG time. The average time in the pool is about twenty-six months.

I’ll write more about the adoption process in a future post. It was just time to disclose what our “special project” was since it represented 39 percent of our spending over the last three months. For the record, the most expensive part of the project is done. However, we are working on acquiring things for our little person (LP), so the kids category is here to stay.

The Colorado housing market

It’s no surprise, but housing in Colorado is costly. The 18 percent that we spent on housing includes the rent and other home supplies (some holiday decor and the stuff that you need to keep a home clean).

Our lease is ending in May and we are already thinking about our next steps. Mr. Smith and I love living here and we’re going to make Colorado our permanent home. We’re thinking and casually looking for a home to purchase, but at the same time aren’t in a rush. More to come on that front as we figure it out.

Those boys and getting around

In the last three months, both boys needed to go to the vet for their annual check-ups. As always, Sisko was a champ and has a clean bill of health. He will need to get his chompers cleaned early next year though. Dental hygiene is incredibly important for little dogs because they’re prone to dental disease. They will need to put him under general anesthesia though and that is always a little worrisome.

Scooter, on the other hand, had his best check-up ever! It was pretty funny though. Mr. Smith went with us because Scooter clocks in at 18.5 pounds and he can be quite difficult to maneuver with his kennel. Mr. Smith waited for us in the lobby while he got his check-up done. The vet walked in as I was unhooking the kennel and exclaimed, “Woah! That’s a big kitty!” The thing is, he is just a large cat. He’s not obese. He just has a very large frame. He got all of his vaccines and we ran his blood work. Everything looks great!

Everything is also in good working order with the car, which is why I’m including it here. We paid the car payment as usual and paid for six months of insurance. No big deal. We did have an unscheduled trip to the dealership to have the door lock looked at. It kept intermittently refusing to unlock. The key word is intermittent. However, they did figure out what was going on. Evidently, some of the glue that holds the soundproofing inside of the door had melted and got into the lock. They cleaned it all out and everything is fine now. The tech said it was one of the strangest issues she had seen in a while. The moral of the story, don’t let them send you away just because the issue is “intermittent.”

The actual percentages

This is a little bit less transparent than before because it doesn’t include spending for taxes, health care, or savings into our tax-deferred accounts. All of this happens before our paychecks even make it to us. I think I’ll keep reporting the numbers like this for the time being as our spending from our accounts is what we have the most control over.

As I mentioned in the introduction, we had some income hyjinx over the last few months. As you know, we moved to Colorado because Mr. Smith got a new job. However, the new job was a poor fit for reasons I’m not going to get into here. In addition, Mr. Smith’s previous employer agreed to a 100 percent remote position. It’s a work in progress, but we like where we are right now.

FI progress

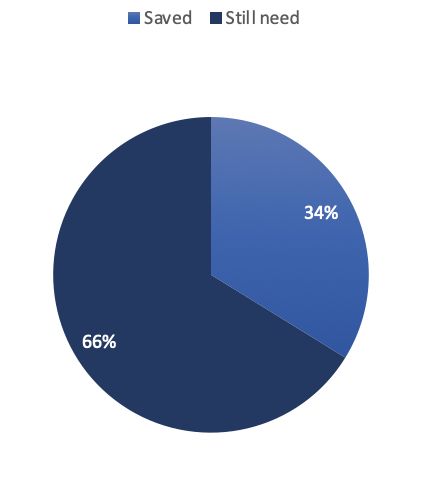

It has been an interesting couple of months in Smithland, to say the least. Compare the percentage saved from this month to our last report, you see that we actually went backwards by 4 percent. There are a couple of factors impacting this. First, we pulled the costs associated with the adoption process from our existing assets. Second, the stock market took a bit of a wild ride over the past few months. We have continued to max out our tax-deferred retirement accounts, but are basically holding even. I’m not worried about things at all. The point of investing is doing it for the long-term and not letting a few blips set you back.

In terms of our savings rate, not surprisingly it is negative given the transfers from savings that we did to pay for the costs of the adoption and the job change hijinx. Things will be smoothed out and back to normal by the beginning of the year.

How did you do this month? Were you able to meet your goals?

4 thoughts on “journey to fi: september 2018 to november 2018 spending report”

Squeeeee! The news is out!I'm saving up for all the trips I'll be taking to Denver. I like your pie charts. I like pie, let's face it. I totally understand the use of percentages vs. $$ amounts. I saw an interesting news story last night. They covered this man who is freaking 80 years old and working at Walmart as a greeter because the large corporation he worked for 29 years laid him off along with hundreds of other people. Somehow his retirement account went in the shitter, his wife got sick, and he is still working to make ends meet. They reported that is costs the average couple $4,100 a month to live (in Oklahoma???). Criminy sakes. How do people do it???? I think health care is something to really keep an eye on and to stay as healthy as humanly possible. Health care is a budget killer, no doubt about it.Okay, gonna go eat rice and beans now. love you! mom

The news is sort of out. We're still not FB official. :)We also like pie. Can you believe that hubby's work mailed him a pie from Michigan last week? I mean, who does that?!I saw a headline for the same story, but didn't read it yet. The Economic Policy Institute (EPI) released a report in 2016 about retirement savings (https://www.epi.org/publication/retirement-in-america/#chart1). Chart 5 is terrifying. The median retirement savings of those aged 56-61 is $17k. That's it!Enjoy your rice and beans!

Thanks! The craziness of the semester got to me and something had to give. I'll be back for the foreseable future. I was even planning out my 2019 blog schedule the other day!

Squeeeee! The news is out!I'm saving up for all the trips I'll be taking to Denver. I like your pie charts. I like pie, let's face it. I totally understand the use of percentages vs. $$ amounts. I saw an interesting news story last night. They covered this man who is freaking 80 years old and working at Walmart as a greeter because the large corporation he worked for 29 years laid him off along with hundreds of other people. Somehow his retirement account went in the shitter, his wife got sick, and he is still working to make ends meet. They reported that is costs the average couple $4,100 a month to live (in Oklahoma???). Criminy sakes. How do people do it???? I think health care is something to really keep an eye on and to stay as healthy as humanly possible. Health care is a budget killer, no doubt about it.Okay, gonna go eat rice and beans now. love you! mom

LikeLike

The news is sort of out. We're still not FB official. :)We also like pie. Can you believe that hubby's work mailed him a pie from Michigan last week? I mean, who does that?!I saw a headline for the same story, but didn't read it yet. The Economic Policy Institute (EPI) released a report in 2016 about retirement savings (https://www.epi.org/publication/retirement-in-america/#chart1). Chart 5 is terrifying. The median retirement savings of those aged 56-61 is $17k. That's it!Enjoy your rice and beans!

LikeLike

Glad you are back Amanda….I missed your posts! (susan’s friend Kathy)

LikeLike

Thanks! The craziness of the semester got to me and something had to give. I'll be back for the foreseable future. I was even planning out my 2019 blog schedule the other day!

LikeLike