Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time. Most months, I report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often see general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income.

I use Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

Without further ado, here’s where we ended up at the end of May 2020.

food and dining expenses

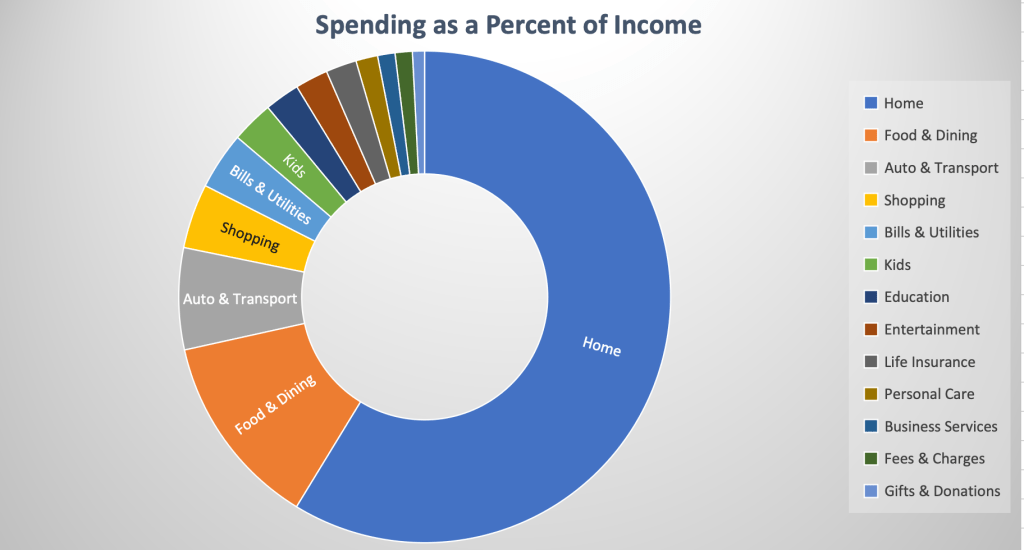

Our food and dining expenses made up 13 percent of our income and 18 percent of our spending.

May was our second most expensive month of 2020, but we’re still on track to spend much less overall than we did in 2019. This month’s food expenses included our weekly food box delivery of eggs, bread, and produce and our weekly Whole Foods delivery. We also did some long-term stocking up with a Nuts.com order that contained lots of our commonly used spices and Amazon Subscribe & Save for pasta, olives, and powdered peanut butter.

I’m a total convert to grocery delivery now. Even after all of this goes back to normal (or whatever semblance of normal we carve out even though I don’t want things to be “normal” again — can you tell I’m working through some stuff?), I don’t think that we’ll go to the grocery store for our weekly supplies any more. It’s just too easy too to put the order in the morning and have the groceries arrive a few hours later. Now, there have been a couple of hiccups. The shopper usually lets me know when an item I want is out of stock and suggests a replacement. Last week, we had burgers on the menu so I had ordered buns. The ones I wanted weren’t available so the shopper suggested brioche buns — a no go due to my allergy. I declined the substitution and decided to try my hand at making English muffins. They weren’t perfect, but they certainly fulfilled their purpose.

auto & transport

Transportation made up 7 percent of our income and 9 percent of our spending.

Since we paid off the car in April, I’ve decided to add it back into the discussion of our top three expenses. This month we paid our six months of car insurance premiums and bought one tank of gas. We pay our car insurance in full every six months so that we don’t have to think about it much and we save a little money by not doing installments. Our insurance provider is refunding 20 percent of April and May premiums so we go a little money back. April’s refund was directly applied to our renewal and May’s will be credited to my credit card.

Since we drive so little now because neither of us commute and LP isn’t sixty miles away in the NICU, we decided to redo our snap shot discount. If you’re not familiar, it’s super easy. You put the device in your car and for six months it tracks your driving. It mainly looks for late night driving, hard brakes, and fast accelerations. Based on how you do, you may get a discount.

shopping

Shopping made up 4 percent of our income and 6 percent of our spending.

Almost all of our shopping was for kitchen things this month. I guess it makes sense since we spend most of our time in the kitchen and it’s reflected in our food spending as well. This month we bought a blender, a juicer, a food scale, a French press, a slotted spoon, and a utensil holder for the counter. Oddly, with the exception of the last two items, all of these were replacements for things that had broken and that we actually use on a regular basis.

I feel like we’ve been much more mindful about our shopping spending this year. There was a time when we would just head to Amazon every time we thought we needed something. We’ve been trying to shop less at Amazon and more locally which means thinking a bit more carefully about what we spend our money on.

the actual percentages

This was a mostly normal income month for us. Justin got his usual two paychecks. We also got our federal tax refund and baby boy’s social security check. As a reminder, I categorize that check as “kids” and it usually offsets spending we do for him. (I’m going to do a post pretty soon about the subscription services that we use for him as there are several that I love.)

As usual, the “home” category is the largest part of our spending. This includes our mortgage, HOA dues, and home maintenance (looking at you 16 bags of mulch).

progress to fi

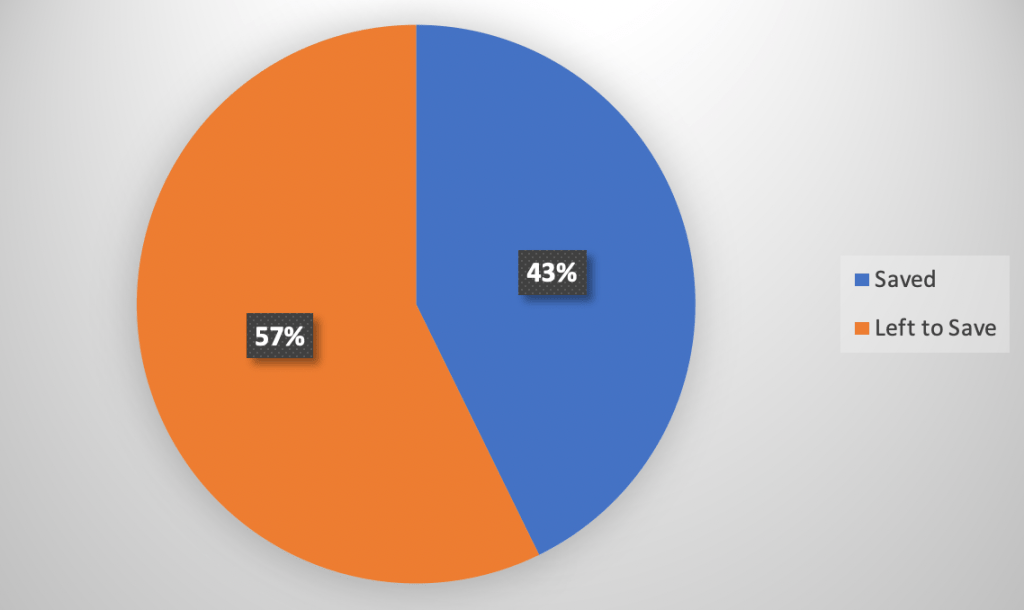

As of this month, we are 43 percent of the way to our fi number. This is 3 percent higher than last month. Our assets have bounced back to where they were pre-COVID. We’re going to continue keeping an eye on the situation, but as I’ve said before, we’re long-term investors. Since we don’t plan on using this money for many years yet, we plan to ride out the market and continue with our investment strategy.

How did your month go? Were you able to achieve your financial goals?