Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time. Most months, I report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often see general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income.

I use Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

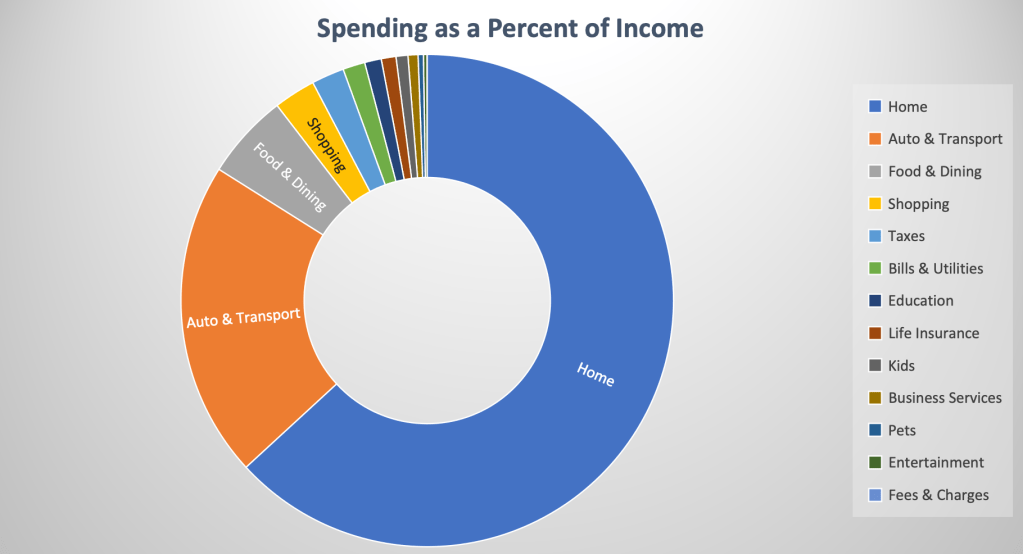

Without further ado, here’s where we ended up at the end of April 2020.

food and dining expenses

Our food and dining expenses made up 4 percent of our income and 6 percent of our spending.

We’ve gotten into a groove in the last month with our grocery shopping. Every Friday our CSA delivers a loaf of bread, 1.5 dozen eggs, a head of lettuce, and an assortment of fruits and vegetables. Once we get the delivery, we sit down and figure out that week’s meal plan based on what else we have in the pantry. We make a Whole Foods delivery order for anything else that we may need that week. This system has helped us to cut back on impulse purchases, reduced our overall food spending, and helped us to reduce food waste.

I should note, savory oatmeal is odd. I was really hoping to like this more than I did because we have lots of oatmeal and sweet oatmeal doesn’t do it for me. I’ll try again and see if I can make some tweaks to make this taste better.

We’ve been using any extra room in our food budget to resupply our pantry. At the end of the month we put in an order with nuts.com for flour, salt, popcorn, and vital wheat gluten. Even with my increased baking, these purchases should carry us through the rest of the year. One thing this pandemic has taught me is that there is A LOT of value in a well-stocked pantry!

We were about $250 below our 12-month average and it was our fifth month, out of the earlier twelve, keeping our total food spending below $1,000. We’re still on track to meet our goal of keeping food costs at 10% or less of our yearly spending.

shopping

Shopping made up 2 percent of our income and 3 percent of our spending.

For people stuck at home, we sure did a lot of shopping this month. Our big purchase was two new wooden cutting boards. We decided it was time to retire our used and much abused plastic cutting boards that we’ve had for almost 10 years. They are both perfect for our needs. (Side note: I also learned that breakfast boards are thing.)

Another big part of our shopping spending was an electronics organizer for my end table. I was tired of playing the charger hokey pokey and found a solution to charge all my gadgets at the same time. It really is the little things.

taxes

Taxes and tax prep made up 2 percent of our income and 2 percent of our spending.

I finally took the time to finish up our 2019 taxes. We ended up filing federal, Colorado, Michigan, Lansing, and Flint taxes this year. Thankfully, we’re done filing in Michigan (and the cities) after 2019.

Overall, we’re getting a pretty hefty tax refund, but we needed to pay for TurboTax and ended up owing the State of Michigan $120.

the actual percentages

We got paid Justin’s annual bonus in April and the spending from that, plus his regular paychecks is included in the percentages below. In addition, we got a check for baby boy from social security that I categorize as “kids” and it usually offsets any spending that we do for him throughout the month.

You’ll notice that our home spending and auto & transport spending were much higher than usual. This is due to bonus spending. We sent $7200 to the mortgage and paid off our car. It feels really nice to not have a car payment again.

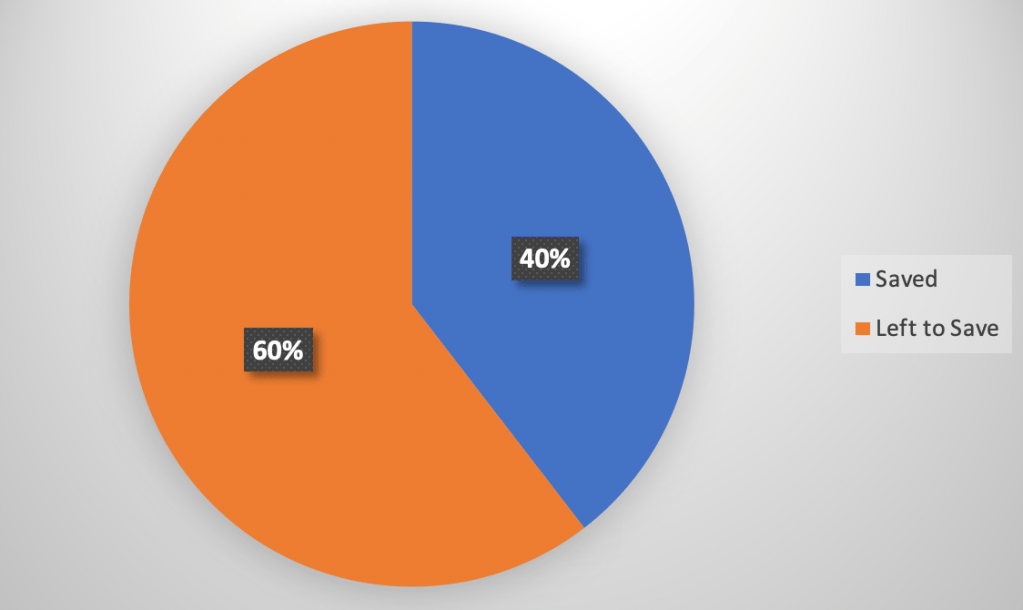

progress to fi

As of this month, we are 40 percent of the way to our fi number. This is 5 percent higher than last month. Our assets have mostly bounced back to where they were pre-COVID. We’re going to continue keeping an eye on the situation, but as I’ve said before, we’re long-term investors. Since we don’t plan on using this money for many years yet, we plan to ride out the market and continue with our investment strategy.

How did your month go? Were you able to achieve your financial goals?