Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time and now feels like the time that increased accountability through reporting our monthly finances. Every month, I’ll report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income. In addition, I’m not quite ready to discuss our actual numbers as I think that both detracts from what we’re trying to do and I want our story to be a bit more approachable.

I used Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.” Without further ado, here’s where we ended up at the end of February 2020.

gifts and donations

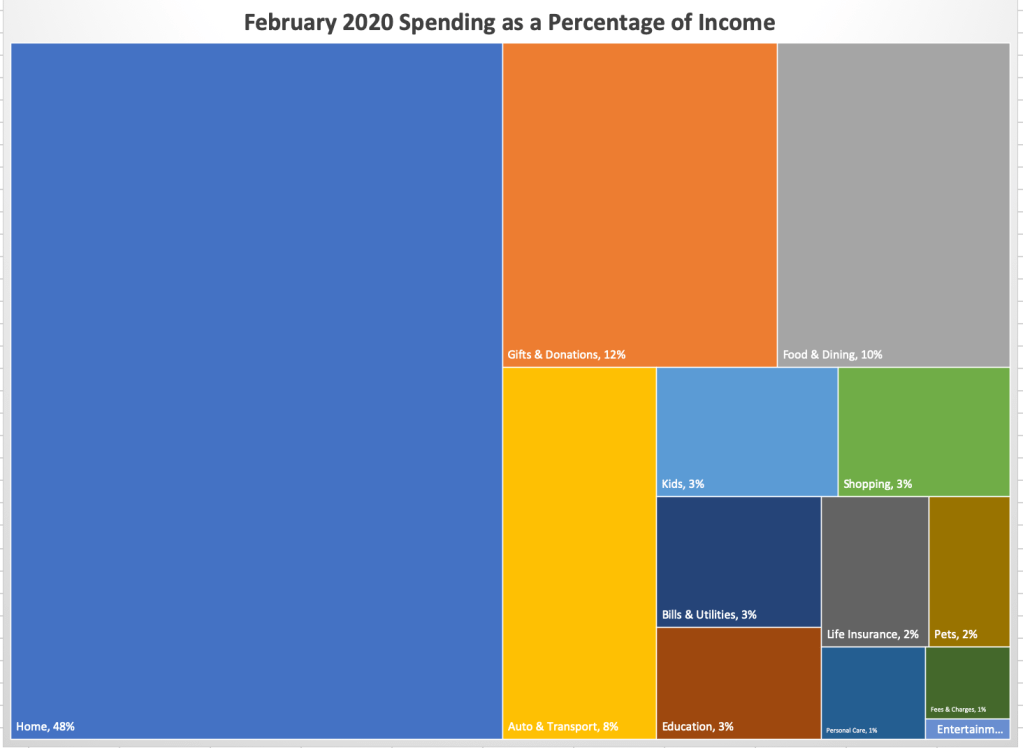

Gifts and donations made up 13 percent of our spending and 12 percent of our income.

My birthday was in February and Justin decided to surprise me with some fancy French cookware that I’ve been eyeing for a long time. This was a planned expense that we completely cash-flowed. We both love cooking with our new pans.

food and dining expenses

Food and dining expenses made up 11 percent of our spending and 10 percent of our income.

Overall, we came 30 percent (!) under budget for the month of February. We were able to save money by creating a meal plan and sticking to it and continuing our meat-free eating. We only ate “out” one time. I put the out in quotations because Justin picked up sushi for my birthday after we put baby boy to bed for the night. Let’s be real. We’re not eating out for a while yet.

kid, shopping, bills & utilities, and education expenses

Kid, shopping, bills & utilities, and education expenses were tied at 3 percent each for our next largest spending category. Collectively, they made up 13 percent of our spending and 12 percent of our income.

We didn’t buy much for baby boy last month. It was mostly medically related things like the stickers that hold the oxygen tube to his face. One of our favorite clothing shops was running a good sale on summer clothes so I stocked up for him. After doing a quick inventory, all I need to get at this point are some pants and shorts in neutral colors to go with all of his tops. I must say that I’m a HUGE fan on kimono-style onesies. I don’t talk a lot about his medical challenges, but the kimono-style onesie makes accessing his feeding tube a lot easier than the ones the snap at the bottom only.

Bills and utilities included our cell phones, water, and electricity bills. These have all been relatively stable since moving to the new house. We did see an increase in the electricity and water bill from when we lived in the apartment, but nothing too dramatic. We’re planning on researching solar panels later on this year for possible installation in 2021.

Lastly, we had our usual contribution to little boy’s 529 plan. We’ve been contributing to it since we decided to adopt — about 2 years before we were actually matched with him. We don’t plan on funding his entire college education, assuming that he goes, but he’ll have a good start on paying for it.

the actual percentages

We only include paycheck spending in this section. This means that the money that comes out of our HSA for various medical expenses isn’t included here. (Fun fact: We’ve already hit our deductible for the year, but that’s for another day.)

progress to fi

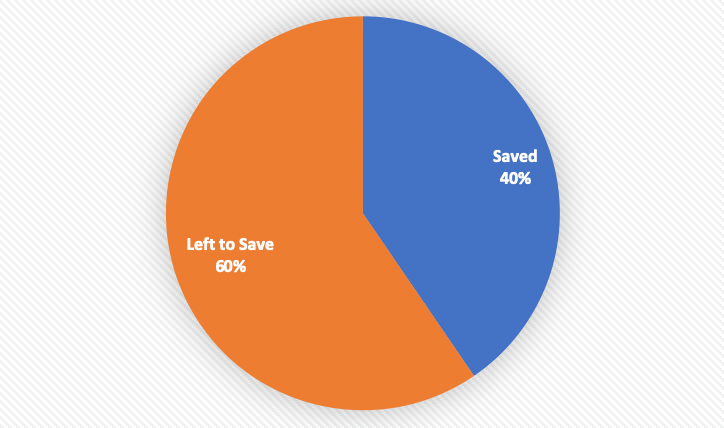

As of this month, we are 40 percent of the way to our fi number. This is four percent lower than last month. The big issue was fluctuations in the market due to fears about coronavirus. We’re long term investors though, so we haven’t made any changes based on this latest market dip. Nothing really major happened this month in terms of our savings. We put the normal amount in and didn’t need to pull anything out for major (and planned) expenses.

While I like how nice and clean this looks, I’m starting work on a new post about our “buckets” saving strategy for FI. More to come soon.

How did your month go?