Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time. Every month, I report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often see general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income.

I use Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.”

I’ve been publishing these monthly spending reports since June 2018. Typically, I talk about our three highest areas of spending (usually housing, food, and transportation), share all of our spending percentages by category, and then talk about our progress towards our FI number. I think it’s time to change things up a bit. Going forward, I’ll discuss our top three expenses with the exception of housing and transportation. These two categories make up a fairly large chunk of our spending and I don’t see that changing any time soon. Frankly, it’s boring and I think the other parts of our spending that are variable are much more interesting to talk about. Justin and I are planning a joint post about our decision-making process on the house after we close.

Without further ado, here’s where we ended up at the end of June 2019.

food costs

Food expenses made up 20 percent of our spending and 16 percent of our income. As I talk about more in the next section, I categorize food eaten while traveling as travel since it’s outside of the norm. That being said, June was a good month for us. We spent less in June than we did in May by about $250 and about $130 less than our 12-month average. We’re also on track to meeting our yearly food spending goals. Compared to the previous 12 months, we’ve spent 12 percent (!) less. We’re not quite where I want to be yet, but I’m hopeful.

During June, we had out-of-town visitors for three days. We did our fair share of eating out and showing them our favorite places to eat. Justin’s mom treated us to dinner for his birthday. We also did a lot of cooking at home. Justin makes an amazing shrimp etouffee and he made it for them. Shrimp isn’t the cheapest ingredient, but totally worth it for this special meal.

The biggest blow to our food cost budget was our 10thanniversary dinner. We decided to go to a super fancy sushi dinner to celebrate and, while delicious, it certainly hit our pocketbook. We decided to go to sushi because that’s what we did the night we got married. It was a fun throwback!

I’m working on our meal plan for July. It’s looking super promising!

travel expenses

Travel expenses made up 6 percent of our spending and 5 percent of our income.

We spent the first part of the month in Bermuda and then I spent a week in Michigan towards the end of the month. You might be wondering why these numbers aren’t as high as you might imagine. First off, Justin’s work reimbursed us for the 80 percent of the Bermuda costs because we were primarily there for his conference. All we needed to pay for this month was my food and our share of the hotel. (Note: I code food eaten while traveling as travel since we’re usually eating out and wouldn’t normally do that at home.) Combining business with pleasure made it so we could have a reasonably affordable trip.

My trip to Michigan was similarly affordable. All I needed to pay for was three days of the rental car and food because I stayed with a combination of friends and family. I’m super thankful that they were willing to let me stay. We set aside money every month for the purpose of travel and were mostly able to cover this month’s adventures from that account.

I’m expecting July to be a bit more expensive in this area as I am paying for the rest of the Bali trip. After looking at the calendar and the sequence of events, I don’t think that I’ll be completely able to travel hack the flights. However, I did find out that I can transfer Marriott points to my United account. I need to explore this a bit more, but that gives me some hope. Once this trip is paid for, we’ll be done (with the exception of maybe one more trip to Michigan) for 2019. All that will be left is to enjoy the trips and make memories. We purposefully planned a lot of travel during 2019 because of the unpredictability of the adoption process. We won’t be doing nearly this much traveling in 2020.

pet care

Pet care made up 4 percent of our spending and 3 percent of our income. I love my boys and taking care of them costs quite a bit of money lately. These figures would be higher if I included pet rent here, but I don’t split out the costs associated with housing.

This month we needed to renew their licenses. The City and County of Denver requires that all cats and dogs be licensed. I can get behind this because the money from the licensing goes towards handling the stray cat population through trap, neuter, and release programs and the upkeep of our dog parks. It also increases the chances that Sisko will find his way back to us if he were to get lost because they have his microchip number. (Scooter is a strictly indoor cat and not microchipped.)

We’ve settled into a medication routine for Scooter. His monthly medication costs were about $50. He seems much more comfortable now that we’ve found the right combination of medications for him. He’ll be on these for the rest of his life. You might be wondering why we’re going this route instead of putting him down. Scooter’s condition is degenerative, and it will get worse over time. However, as long as we can keep him comfortable and functioning, we don’t see the point in ending his life. For some, the cost of $50 forever might be daunting or too much, but he’s part of our family and this is what you do for family. There will come a point when we can’t keep him pain-free and/or his quality of life will decrease. When that time comes, we’ll make the decision.

We also needed some basic pet supplies of dog food and litter boxes and Sisko needed to have his nails trimmed. Grooming is one area that we could do ourselves but have made the conscious choice to outsource. We do handle Sisko’s baths, but don’t do his nails any more. Little buddy turns into the Hulk when we try to do them and it’s traumatic for all involved. No thank you. The last time we did them, over a year ago, all three of us ended up taking a nap afterward because we were spent.

the actual percentages

Below are the rest of the month’s spending percentages. Our home and transportation expenses made up 41 percent of our total spending for the month. This has been the same for quite a while. If you add up the the percentages, you’ll notice that our spending did not equal 100% of our income this month. We had about 19% left over that went towards savings.

progress to fi

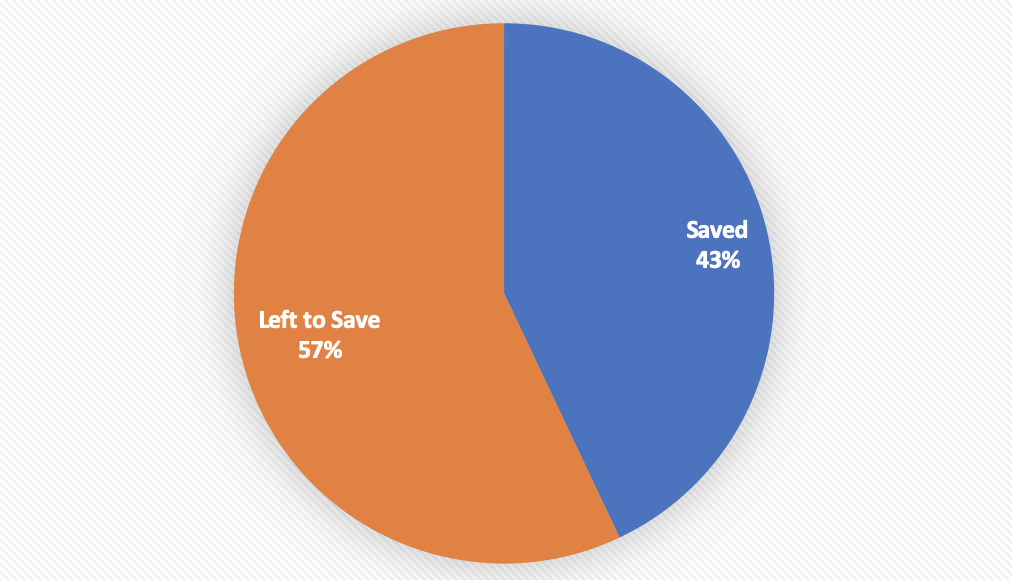

As of this month, we are 43 percent of the way to our fi number. Most of these gains were from the market bouncing back a bit from May’s less than stellar perfomance. I fully expect our progess to decrease when we close on the house since our downpayment money is included here for the moment. I like to report the numbers as they are, even though I know that there are changes on the horizon.

I got my last paycheck from the University this month and my last retirement contributions will post in a few days. Starting in August, our savings rate will probably slow down a bit since I won’t be saving all of my income every month any more. We aren’t worried about this though. At this point in our journey, we’ve saved enough in our retirement accounts to not need to add another dime to them. They’ll keep growing and will be sufficient when we’re old enough to draw from them penalty free. At this point, we’re more focused on building the bucket that will get us from the time Justin retires to 59.5 years old.

How did your month go? Were you able to achieve your financial goals?