A major part of the financial independence journey is protecting your assets. Since Justin is an actuary, it only makes sense for him to be the one to write about this stuff. Let us know what else you would like to learn about in the insurance world in the comments below. As a reminder, none of this is to be taken as financial advice.

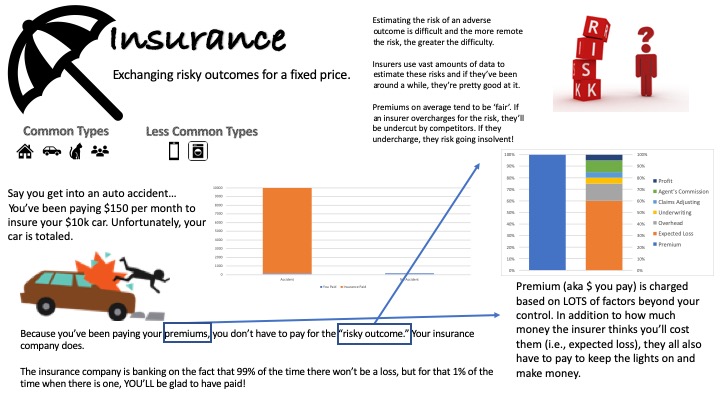

Purchasing insurance can be intimidating, but all insurance boils down to exchanging an uncertain outcome for a certain one for a premium.

Uncertain Outcome + Insurance => Certain Outcome

Let’s say you own a car worth $10,000 and for $150 your auto insurer will cover your losses in the instance of a collision up to the full value of the car.

To make things simple we’ll assume there are only two possible outcomes:

- 99% of the time there is no loss.

- 1% of the time there will be a total loss of $10,000.

On average, the collision damage to your car will cost 0.99*0 + 0.01*10000 = $100.

Purchasing insurance makes all outcomes the same regardless of what happens, let’s look at that now:

- 99% of the time there is no loss and we pay $150 in premium.

- 1% of the time there is a total loss, we pay $150 and the insurer picks up the remaining $9,850.

In all cases we’re out the premium of $150. In the most likely scenario we are “down” $150 against no loss, in the unlikely scenario we are “up” $9,850 compared to having no insurance.

Wait! Where’d the extra $50 go?

Hard to pull a fast one on you. In addition to paying for your expected loss, the insurer has to pay for their expenses. These include, but aren’t limited to:

- Overhead (e.g. their office building).

- Underwriters to bind your policy.

- Claims adjusters to handle claims.

- An agent’s commission.

- A profit provision for the insurer.

The typical percentage of premium that goes to paying losses is around 40-60%, though this can vary widely by the type of coverage. The remainder goes to covering expenses and profit.

I didn’t have a loss, I would have been better off not buying insurance at all!

Something to keep in mind when reflecting on insurance purchases where no claim was made is that you only could have known that after the fact. It’s important to note that insurance trades futureuncertainty for a fixed outcome today, you necessarily cannot buy insurance to cover an event that is certain to occur at a certain time and with a certain cost.

So whether the insurance is worth it comes down to whether you could have financially weathered the worst outcome (a total loss of $10,000 in our example above). If the answer is no, then keep in mind that not purchasing the insurance would have exposed you to a potentially devasting loss.

I feel like I’m offered insurance on everything these days, how do I know which to buy and which to pass on?

The answer to this question is going to vary for each individual, because not every person will bear loss the same way. The price of insurance will necessarily exceed the expected value of the losses covered (otherwise no insurer could stay in business), but that doesn’t necessarily make insurance a ‘bad deal’.

When considering the purchase of insurance ask yourself: what is the worst-case scenario this insurance covers and how would my family’s financial fortunes be impacted?

If you’re offered a warranty on a new video game for $2 (yes, this is a real thing) what risk are you covering? The ‘total loss’ scenario is that the game will become scratched and you will have to buy a new copy. In this case a total loss is around $60, which most people could reasonably cover out of pocket. This ‘inexpensive’ coverage isn’t a bargain after all.

You may scoff at purchasing a warranty on a game disc, but have you purchased a warranty on a vacuum cleaner or a microwave? Policies for household appliances are big money for insurers and they’re happy to take on your risk for a premium. If the losses covered are moderate ($100-$1000), my recommendation is to ask what the premium will run you and then set that amount aside for a rainy day. Over the long run the premiums you collect are likelyto cover any losses you incur with a bit left over.

It’s important to note here that not every family can absorb an unexpected $1,000+ loss! Please keep this in mind as you weigh the pros and cons of purchasing a coverage for an expensive home appliance or travel insurance for the trip you’ve saved five years to take.

On the other hand there are insurance coverages which you may find cover a remote, but financially devasting outcome. Some examples include:

- Term life insurance and disability insurance for the primary earner of a family of six.

- Long-term care insurance for yourself or an aging relative.

- Optional collision coverage for an expensive personal vehicle.

In conclusion insurance trades an uncertain outcome for a certain one, but at a price. When purchasing insurance keep in mind whether you’re willing to retain the risk of an unfavorable outcome. If you are, it may make sense to pass on the coverage. If not, insurance can be an excellent way of transferring the risk over to another party.

One thought on “a crash course in insurance”