Mr. Smith and I have a dream of achieving financial independence (FI). We’ve been on this path for quite some time and now feels like the time that increased accountability through reporting our monthly finances. Every month, I’ll report the percentages that we spent in each category, our savings rate for the month, and our progress towards our FI number.

You might wonder why I’m reporting percentages and not the actual numbers. Personally, I think that percentages make a lot more intuitive sense for most people. For example, we often general financial rules expressed as percentages such as the rule that your housing expenses should be no more than 30 percent of your gross income. In addition, I’m not quite ready to discuss our actual numbers as I think that both detracts from what we’re trying to do and I want our story to be a bit more approachable.

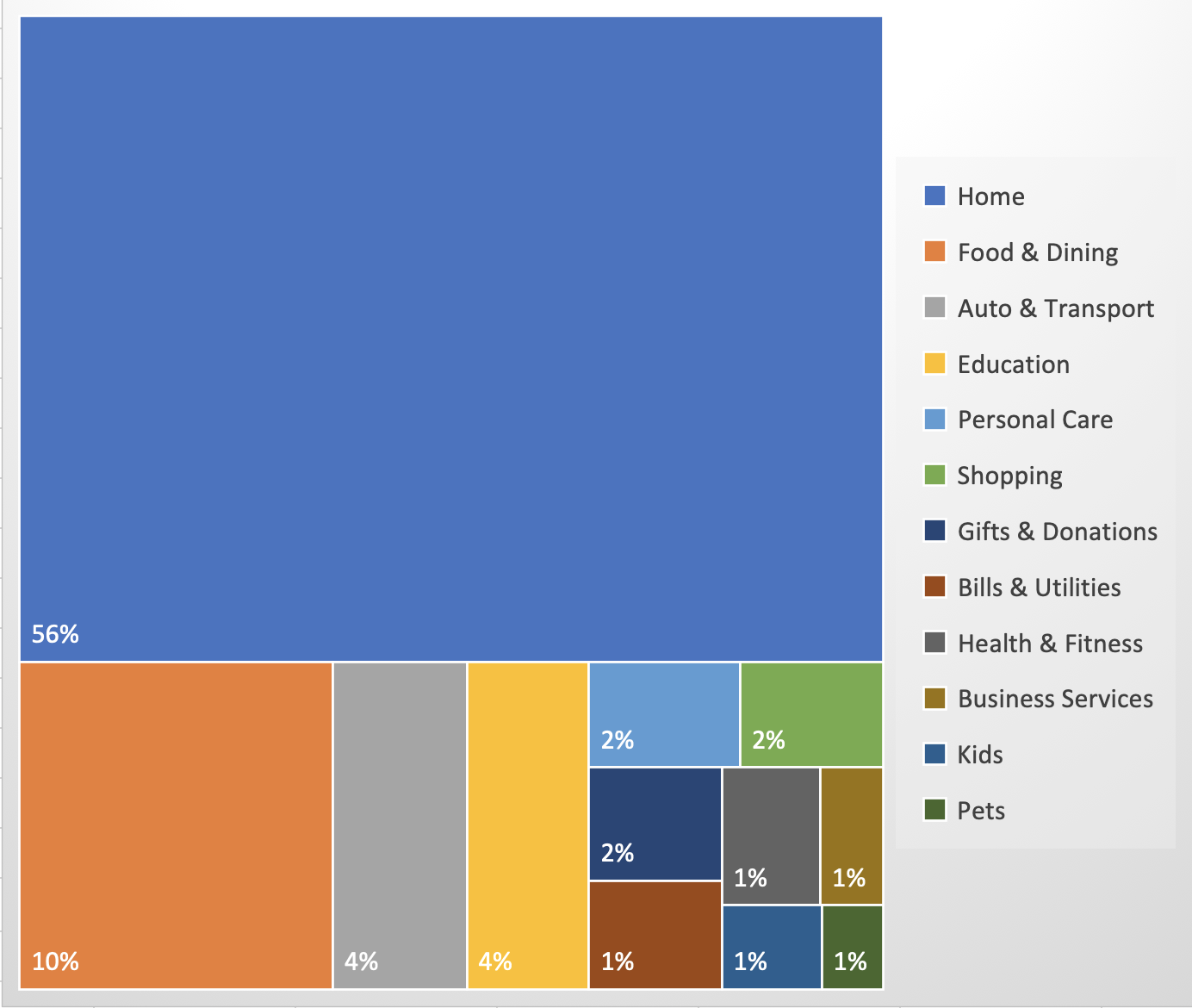

I used Mint to generate the spending report and figure out our current net worth. It’s not perfect, but as Mr. Smith likes to say, “Don’t let the perfect be the enemy of the good.” Without further ado, here’s where we ended up at the end of December 2018. I do a separate post about our 2019 goals soon.

more big changes are in the works

Since moving to Colorado, Mr. Smith and I have had our eye on the real estate market. We love living here very much and want to make it our permanent home. Our lease is up in May and it was important for us to start thinking about our next move.

One thing that we noticed about the market is that new builds seem to cost about as much as existing builds. So, we decided to see what the new builds have to offer and if one could meet our needs. For us, the draw of a new build is that the home is exactly how you want it, you know the home’s history, and there is usually a warranty. With all of that being said, Mr. Smith and I found the right home for us and put down our earnest money/part of the downpayment this month. They haven’t broken ground yet, I will write more about how the house will impact our FI goals later on.

food remains one of our biggest line items

Not surprisingly, food and dining continues to be the second largest percentage of our monthly spending. This month it made up 10 percent of our monthly income. There were two big meals that were out of the ordinary this month. We hosted Christmas Eve eve brunch for some friends and I made an over-the-top roasted lamb dinner for the two of us for Christmas. However, this isn’t completely out of the ordinary as I usually do one or two big meals every month.

I mentioned in my grocery shopping post that I’ll be handling grocery shopping in the near future as I transition away from paid work. It’ll be interesting to see what happens then. I don’t think I’ll be any better at grocery shopping than Mr. Smith, but we’ll see.

transportation costs remain stable

Our transportation costs include the car payment and gas. Since Mr. Smith has transitioned to working 100% remotely, we drive MUCH less frequently. This month, we only needed to get gas twice and gas prices have been going down here. Transportation costs were 4 percent of this month’s income.

This is a much welcome change from our time in Michigan. Once we moved back to town, Mr. Smith was able to walk to work again and we downsized back to one car. However, I still needed to be on-campus three to four days per week and it was a 90-mile round trip commute. Needless to say, I don’t miss it one bit.

education expenses

We also spent four percent of this month’s income on education. Since deciding to embark on the adoption journey, we have contributed to a 529 plan. The 2018 tax changes made this a bit more reasonable for us because now you can use 529 money to pay for k-12 expenses as well. We’re not sure what route we’ll take with educating our little person, but having options is nice.

We also pay for my sister’s school books. She’s entering her second semester at University and the last thing I want her to stress out about is the cost of books, which, by the way, is a racket. It’s been a while since I’ve purchased an undergraduate textbook for myself and I was astounded when I saw how much one of her textbooks would cost at the University bookstore. On the upside, I’m a pretty savvy shopper and managed to find most of her books at a reasonable-ish price. (I think I’m sensing another post idea.)

the actual numbers

journey to fi

December was a rough month for us (and many other people). The stock market continues to be shaky with Christmas Eve being particularly bad. I try to make a habit to not actually look since investing is about the long-term plan and not the day-to-day fluctuations. That, plus putting down part of our downpayment, caused us to drop two percentage points from our fi goal. It’s not the end of the world.

How did your month go? Did you meet your goals?